ECB: Insights into the digital transformation of the retail payments ecosystem

![]() Autor: Bancherul.ro

Autor: Bancherul.ro

2018-01-12 10:13

“An idea that is not dangerous is unworthy of being called an idea at all.”

The above quote by Oscar Wilde resonated throughout the conference that the European Central Bank and the Banca d’Italia hosted on 30 November and 1 December 2017 in Rome. Entitled “Digital transformation of the retail payments ecosystem”, this conference looked in detail at the dynamic developments that are currently being observed in the retail payments industry on account of new technologies and changes in consumer demand.

This event brought together nearly 300 participants from 53 countries around the world and featured policy discussions on issues such as innovation, interoperability and the integration of retail payments, as well as cybersecurity in the financial ecosystem. The speakers at this conference included the authors of eight academic papers on virtual currencies, the adoption of instant payments and customer behaviour, who presented their findings to participants.

This article seeks to provide an overview of the key messages conveyed by the event’s various high level guest speakers, who hailed from both the financial industry and academia.

An introduction to the subject of innovation

The conference was opened by Ignazio Visco, Governor of the Banca d’Italia, and Yves Mersch, a member of the Executive Board of the ECB, both of whom emphasised that an appropriate legislative framework and cooperation between all stakeholders was key to supporting innovation and ensuring the security of the retail payments ecosystem.

In his welcome address, Mr Visco described the retail payments landscape as “highly dynamic” and “ever-evolving”. He warned that the rapid digital transformation being observed in the industry posed a number of challenges to central banks, one of which was the need to adapt the regulatory framework in order to support innovation. He argued that, in the European context, the revised Payment Services Directive (PSD2) would pave a stable path towards further innovation. Another challenge concerned the oversight of payment systems and payment instruments that were based on new technologies. Central banks needed to be at the forefront of innovation in order to be able to assess vulnerabilities and ensure cybersecurity in the financial ecosystem, he said.

Drawing on the ECB’s experience with the Single Euro Payments Area (SEPA), Mr Mersch pointed out that another key ingredient when rolling out payment innovations was stakeholder involvement. He cited the example of the Euro Retail Payments Board (ERPB), which had brought together stakeholders from both the supply and the demand side of the market and had been instrumental in the emergence of pan-European instant payments in euro. Mr Mersch urged banks to implement instant payments in order to remain competitive in a real-time digital world. He also shared his conviction that pan-European instant payments would “provide an alternative narrative to the ongoing public debate on the alleged innovation brought about by virtual currency schemes”, which he said were “not robust enough from a legal, operational and governance point of view” to formally qualify as currencies.

How is digital evolution affecting the retail payments ecosystem?

A panel discussion brought together high-level representatives of central banks on four different continents, who offered valuable insights into the latest global developments in terms of digital evolution. They identified four areas where digitalisation was having an impact on the retail payments ecosystem:

- new players and new technologies entering the market;

the dilution of the various steps involved in the processing of payment transactions;

- increasing demand for universal payment instruments that offer the same speed, efficiency and cost both domestically and globally;

- new risks for infrastructure and settlement assets as a result of new technologies.

What role should central banks play in retail payments innovation?

The panel agreed that the impact of innovative technologies and new market entrants on the retail payments industry was twofold. These new developments could help to increase the security and efficiency of retail payments, but they could also result in financial markets fragmenting again and conflict with central banks’ financial stability objectives.

In this context, the panel argued that central banks should seek to engage the industry in a constructive discussion and adjust the regulatory framework in line with the new digital environment. As regards the development of a cashless economy, panellists said that central banks should promote freedom of choice and allow the market and users to decide whether they preferred cash or electronic payments. In addition, it was felt that central bank-backed digital currencies had not yet been sufficiently explored and could potentially contribute to the emergence of a cashless economy in the future.

How can incumbent banks embrace innovation?

Chris Skinner, a fintech commentator and author, predicted that the banking industry would change dramatically in the next ten years, mirroring the technological transformations that had been observed in a number of other sectors, such as retail and medicine. In this context, incumbent banks would face huge challenges when it came to updating their legacy systems. The digitalisation of back offices had the potential to make millions of jobs redundant and needed to go hand in hand with changes in corporate culture and structure, he said.

Could fintech be the answer? Across the financial industry, many people believe that fintech innovations such as distributed ledger technology (DLT) and artificial intelligence could prove effective in modernising legacy systems and optimising the internal procedures of financial institutions. Others go even further, suggesting that – if widely adopted – these innovations could transform the financial ecosystem as a whole. From today’s perspective, it is hard to predict what the future holds, as most of the current DLT-based solutions are not suitable for broad-based application in the financial industry, being restricted to specific niches.

José María Roldán, Chairman and CEO of the Spanish Banking Association and Vice-President of the European Banking Federation, shared his belief that fintech presents both challenges and opportunities for incumbent banks, explaining that it increases competition, but also allows costs to be reduced and can lead to greater returns on equity. He also emphasised that the banking sector contributed to financial stability and that the rise of fintech companies would not threaten its existence. However, he encouraged banks to gain a better understanding of these new technological developments, to be aware of their own vulnerabilities and to use the information at their disposal to improve the user-friendliness of their services.

A panel looking at the disruptive potential of fintech innovations acknowledged that the nature of competition in the retail payments industry was changing. In order to keep up with fintech innovations, established market players needed to adjust their infrastructure and business models in line with the new environment. Incumbents needed to increase investment in new technologies and cooperate with fintech companies, panellists said.

Instant payments – adoption and interoperability

One of the event’s panellists argued that payments should be “simple, safe and smart”, and the new SEPA Instant Credit Transfer (SCT Inst) scheme is designed to be just that. That new scheme allows funds to be transferred in euro in a matter of seconds, both within and between countries, and gives banks and other payment service providers an opportunity to embrace innovation.

With the “old continent” taking a big step towards pan-European instant payments, a recent comparative study by Monika Hartmann, Lola Hernández, Mirjam Plooij and Quentin Vandeweyer from the ECB asked whether instant payments would become the new normal. That study looked at six countries – both in Europe and elsewhere – where instant payments had been introduced in recent years and identified seven factors which had contributed to their uptake:

- active involvement of relevant authorities;

- cooperation between payment service providers;

- added value in terms of speed relative to legacy systems;

- good pricing conditions;

- presence of complementary services;

- widespread use of internet and mobile data;

h

- igh levels of internet banking.

On the basis of those drivers, the paper concluded that the euro area was in a good position to support instant payments and analysed four different scenarios as regards their adoption.

Looking at the bigger picture, instant payments are becoming increasingly common around the world, and the financial industry now faces the challenge of ensuring international interoperability. Against this background, a panel featuring representatives of three different continents – North America, Asia and Europe – talked about how to overcome this interoperability challenge. Those panellists identified the lack of standardised and harmonised message formats as a major issue, pointing out that this could be solved by aligning legal frameworks and adopting international standards such as BIC/IBAN and ISO 20022. They also recommended increasing international cooperation between regulators, banks and market infrastructures in order to address the inefficiencies of international payments while ensuring privacy and data protection.

Virtual currencies

The subject of virtual currencies – one of the hot topics in the financial industry at the moment – was also addressed, being raised in Mr Mersch’s opening speech and elaborated on in three of the academic papers presented at the event.

In the first of those papers, Christopher S. Henry, Kim P. Huynh and Gradon Nicholls from the Bank of Canada looked at awareness and use of Bitcoin among Canadian citizens. Their empirical study showed that around 64% of Canadians had heard of Bitcoin, but only 2.9% owned it.

Nicole Jonker from De Nederlandsche Bank adopted a different perspective, trying to identify what drives retailers’ adoption of virtual currencies by talking to 43 retailers in the Netherlands. The main reasons for accepting such currencies included a desire to attract extra customers (reported by 42% of retailers that accepted crypto-currencies), a desire to meet specific customer demands (23%) and an interest in new technologies (21%). The main reasons for not accepting them included a lack of familiarity with virtual currencies (58%) and a lack of customer demand (36%).

In her paper, Ruth Wandhöfer from Cass Business School looked at the possibility of introducing a central bank-backed crypto-currency to complement physical banknotes and coins. She examined possible scenarios for the adoption of “euro crypto-cash” and made suggestions regarding its design.

In this context, Professor Silvio Micali from the MIT Computer Science and Artificial Intelligence Laboratory presented a new DLT-based crypto-currency – called “algorand” – which he had developed on the basis of a Byzantine consensus algorithm. Professor Micali felt that this solution boasted real technical advantages in the form of trivial computation and true decentralisation, but its limited speed was considered to be a drawback.

Customer choice and behaviour

The retail payments industry is just one of many sectors where customer behaviour has been shaped by mass access to the internet and mobile phones in recent years. Changes in consumer demand have triggered various new developments, such as user-friendly mobile applications allowing the initiation of payments and innovative customer identification methods.

Two of the academic papers that were presented at this conference looked at customer preferences in different countries as regards payment instruments.

Jan Lukas Korella from the Deutsche Bundesbank compared retail payment behaviour in China and Germany. His study found that banks played an important role in the German payment landscape, as consumers’ preferred payment method at the point of sale was cash (51.3%), followed by card-based payments (45.6%). In China, meanwhile, there was a significant difference between metropolitan and rural areas when it came to preferred payment methods: 56.1% of customers in Chinese megacities used non-bank mobile payments and only 21.5% relied on cash at the point of sale, while cash was still the dominant payment method in rural areas.

Another paper by Tamás Ilyés and Lóránt Varga from the Magyar Nemzeti Bank analysed all payment transactions in Hungary in order to identify the main drivers of card acceptance and usage in the country. Their paper concluded that shops with higher levels of annual revenue were more likely to accept card payments and that customers were more likely to pay by card when the value of the transaction was higher.

With PSD2 requiring payment service providers to apply strong customer authentication methods for remote electronic payments, Guerino Ardizzi from the Banca d’Italia looked at how two-factor authentication methods, such as the 3-D Secure protocol, affect the user experience. Analysing data from Italy, he found empirical evidence of a trade-off between the security of technology and its usability.

Meanwhile, Carin van der Cruijsen from De Nederlandsche Bank looked at the issue of consumer privacy in the context of PSD2, exploring consumers’ attitudes to the use of payment data. The results of a recent survey of Dutch consumers indicate that 60% regard the confidentiality of payment data as important, with most people not wanting to share payment data with non-banks and the majority of consumers regarding the selling of payment data to commercial companies as unacceptable. Her paper concluded that context was important and that details of how data will be used should be clearly communicated to consumers in order to obtain their consent.

Cybersecurity

The increasing digitalisation and interconnectedness of financial services provides opportunities to improve the user experience, but it also poses a threat to cybersecurity.

Cyberattacks have become more frequent and sophisticated in recent years, threatening not only the individual institution in question, but the entire sector and the financial ecosystem as a whole. Against this background, Fabio Panetta, Deputy Governor of the Banca d’Italia, argued that we should “recognise that cyberspace is a global public good” and that responsibility for ensuring its security should be shared between governments, public institutions, private industry and academics. Approaching this issue from a central banking perspective, he said that an effective cybersecurity strategy rested on three pillars: regulation, cooperation and awareness of risks.

In the same vein, a panel moderated by Jan Smets, Governor of the Nationale Bank van België/Banque Nationale de Belgique, agreed that the financial industry needed to show solidarity and cooperate, as cybersecurity was not an issue to compete on. In the course of that exchange of views, a number of suggestions were made as regards the best ways of protecting the retail payments ecosystem and building trust:

- increase spending on security protection (i.e. penetration tests);

- adopt a holistic approach and use dynamic risk

- management to tackle cyberthreats;

- use new technologies to analyse transaction risk and customer behaviour and manage fraud;

- establish an international forum bringing together experts from the world of cybersecurity;

- take steps to address the shortage of cybersecurity experts in the financial industry.

Comentarii

Adauga un comentariu

Adauga un comentariu folosind contul de Facebook

Alte stiri din categoria: Noutati BCE

Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%

Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%, in cadrul unei conferinte de presa sustinute de Christine Lagarde, președinta BCE, si Luis de Guindos, vicepreședintele BCE. Iata textul publicat de BCE: DECLARAȚIE DE POLITICĂ MONETARĂ detalii

BCE creste dobanda la 2%, dupa ce inflatia a ajuns la 10%

Banca Centrala Europeana (BCE) a majorat dobanda de referinta pentru tarile din zona euro cu 0,75 puncte, la 2% pe an, din cauza cresterii substantiale a inflatiei, ajunsa la aproape 10% in septembrie, cu mult peste tinta BCE, de doar 2%. In aceste conditii, BCE a anuntat ca va continua sa majoreze dobanda de politica monetara. De asemenea, BCE a luat masuri pentru a reduce nivelul imprumuturilor acordate bancilor in perioada pandemiei coronavirusului, prin majorarea dobanzii aferente acestor facilitati, denumite operațiuni țintite de refinanțare pe termen mai lung (OTRTL). Comunicatul BCE Consiliul guvernatorilor a decis astăzi să majoreze cu 75 puncte de bază cele trei rate ale dobânzilor detalii

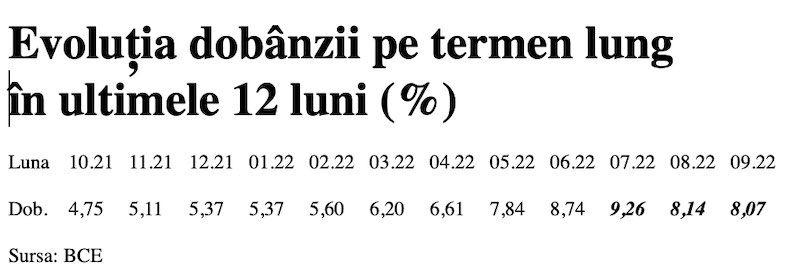

Dobânda pe termen lung a continuat să scadă in septembrie 2022. Ecartul față de Polonia și Cehia, redus semnificativ

Dobânda pe termen lung pentru România a scăzut în septembrie 2022 la valoarea medie de 8,07%, potrivit datelor publicate de Banca Centrală Europeană. Acest indicator, cu referința la un termen de 10 ani (10Y), a continuat astfel tendința detalii

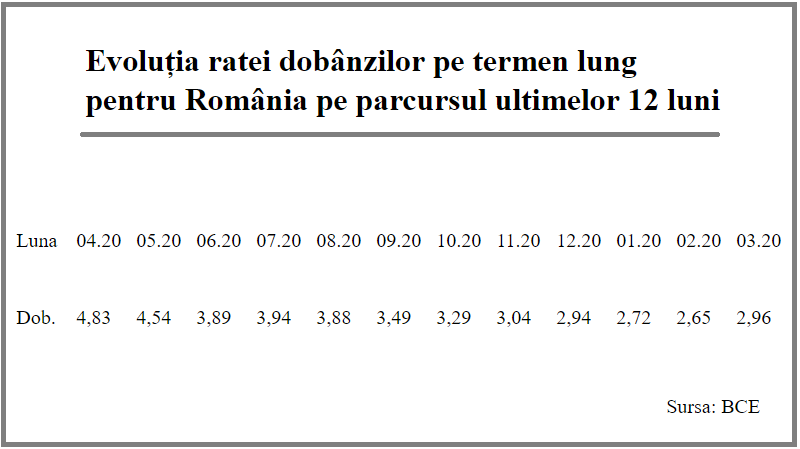

Rata dobanzii pe termen lung pentru Romania, in crestere la 2,96%

Rata dobânzii pe termen lung pentru România a crescut la 2,96% în luna martie 2021, de la 2,65% în luna precedentă, potrivit datelor publicate de Banca Centrală Europeană. Acest indicator critic pentru plățile la datoria externă scăzuse anterior timp de șapte luni detalii

- BCE recomanda bancilor sa nu plateasca dividende

- Modul de functionare a relaxarii cantitative (quantitative easing – QE)

- Dobanda la euro nu va creste pana in iunie 2020

- BCE trebuie sa fie consultata inainte de adoptarea de legi care afecteaza bancile nationale

- BCE a publicat avizul privind taxa bancara

- BCE va mentine la 0% dobanda de referinta pentru euro cel putin pana la finalul lui 2019

- ECB: Insights into the digital transformation of the retail payments ecosystem

- ECB introductory statement on Governing Council decisions

- Speech by Mario Draghi, President of the ECB: Sustaining openness in a dynamic global economy

- Deciziile de politica monetara ale BCE

Profil de Bancher

-

Mihai Lazar, Director Vanzari

Raiffeisen Capital & Investment

martie 2013 - Mihai Lazar se alatura diviziei de ... vezi profil

Criza COVID-19

- In majoritatea unitatilor BRD se poate intra fara certificat verde

- La BCR se poate intra fara certificat verde

- Firmele, obligate sa dea zile libere parintilor care stau cu copiii in timpul pandemiei de coronavirus

- CEC Bank: accesul in banca se face fara certificat verde

- Cum se amana ratele la creditele Garanti BBVA

Topuri Banci

- Topul bancilor dupa active si cota de piata in perioada 2022-2015

- Topul bancilor cu cele mai mici dobanzi la creditele de nevoi personale

- Topul bancilor la active in 2019

- Topul celor mai mari banci din Romania dupa valoarea activelor in 2018

- Topul bancilor dupa active in 2017

Asociatia Romana a Bancilor (ARB)

- Băncile din România nu au majorat comisioanele aferente operațiunilor în numerar

- Concurs de educatie financiara pentru elevi, cu premii in bani

- Creditele acordate de banci au crescut cu 14% in 2022

- Romanii stiu educatie financiara de nota 7

- Gradul de incluziune financiara in Romania a ajuns la aproape 70%

ROBOR

- ROBOR: ce este, cum se calculeaza, ce il influenteaza, explicat de Asociatia Pietelor Financiare

- ROBOR a scazut la 1,59%, dupa ce BNR a redus dobanda la 1,25%

- Dobanzile variabile la creditele noi in lei nu scad, pentru ca IRCC ramane aproape neschimbat, la 2,4%, desi ROBOR s-a micsorat cu un punct, la 2,2%

- IRCC, indicele de dobanda pentru creditele in lei ale persoanelor fizice, a scazut la 1,75%, dar nu va avea efecte imediate pe piata creditarii

- Istoricul ROBOR la 3 luni, in perioada 01.08.1995 - 31.12.2019

Taxa bancara

- Normele metodologice pentru aplicarea taxei bancare, publicate de Ministerul Finantelor

- Noul ROBOR se va aplica automat la creditele noi si prin refinantare la cele in derulare

- Taxa bancara ar putea fi redusa de la 1,2% la 0,4% la bancile mari si 0,2% la cele mici, insa bancherii avertizeaza ca indiferent de nivelul acesteia, intermedierea financiara va scadea iar dobanzile vor creste

- Raiffeisen anunta ca activitatea bancii a incetinit substantial din cauza taxei bancare; strategia va fi reevaluata, nu vor mai fi acordate credite cu dobanzi mici

- Tariceanu anunta un acord de principiu privind taxa bancara: ROBOR-ul ar putea fi inlocuit cu marja de dobanda a bancilor

Statistici BNR

- Deficitul contului curent după primele două luni, mai mare cu 25%

- Deficitul contului curent, -0,39% din PIB după prima lună a anului

- Deficitul contului curent, redus cu 17%

- Inflatia a încheiat anul 2023 la 6,61%, semnificativ sub prognoza oficială

- Deficitul contului curent, redus cu o cincime după primele zece luni ale anului

Legislatie

- Legea nr. 311/2015 privind schemele de garantare a depozitelor şi Fondul de garantare a depozitelor bancare

- Rambursarea anticipata a unui credit, conform OUG 50/2010

- OUG nr.21 din 1992 privind protectia consumatorului, actualizata

- Legea nr. 190 din 1999 privind creditul ipotecar pentru investiții imobiliare

- Reguli privind stabilirea ratelor de referinţă ROBID şi ROBOR

Lege plafonare dobanzi credite

- BNR propune Parlamentului plafonarea dobanzilor la creditele bancilor intre 1,5 si 4 ori peste DAE medie, in functie de tipul creditului; in cazul IFN-urilor, plafonarea dobanzilor nu se justifica

- Legile privind plafonarea dobanzilor la credite si a datoriilor preluate de firmele de recuperare se discuta in Parlament (actualizat)

- Legea privind plafonarea dobanzilor la credite nu a fost inclusa pe ordinea de zi a comisiilor din Camera Deputatilor

- Senatorul Zamfir, despre plafonarea dobanzilor la credite: numai bou-i consecvent!

- Parlamentul dezbate marti legile de plafonare a dobanzilor la credite si a datoriilor cesionate de banci firmelor de recuperare (actualizat)

Anunturi banci

- Bancile comunica automat cu ANAF situatia popririlor

- BRD bate recordul la credite de consum, in ciuda dobanzilor mari, si obtine un profit ridicat

- CEC Bank a preluat Fondul de Garantare a Creditului Rural

- BCR aproba credite online prin aplicatia George, dar contractele se semneaza la banca

- Aplicatia Eximbank, indisponibila temporar

Analize economice

- Rezultatul economic pe 2023, tot +2,1% dar cu 7 miliarde lei mai mare

- România - prima în UE la inflație, prin efect de bază

- Deficitul comercial lunar a revenit peste cota de 2 miliarde euro

- România, 78% din media UE la PIB/locuitor în 2023

- România - prima în UE la inflație, prin efect de bază

Ministerul Finantelor

- Datoria publică, imediat sub pragul de 50% din PIB la începutul anului 2024

- Deficitul bugetar, deja -1,67% din PIB după primele două luni

- Datoria publică, sub pragul de 50% din PIB la finele anului 2023

- Deficitul bugetar, din ce în ce mai mare la început de an

- Deficitul bugetar după 8 luni, încă mai mare față de rezultatul din anul trecut

Biroul de Credit

- FUNDAMENTAREA LEGALITATII PRELUCRARII DATELOR PERSONALE IN SISTEMUL BIROULUI DE CREDIT

- BCR: prelucrarea datelor personale la Biroul de Credit

- Care banci si IFN-uri raporteaza clientii la Biroul de Credit

- Ce trebuie sa stim despre Biroul de Credit

- Care este procedura BCR de raportare a clientilor la Biroul de Credit

Procese

- Un client Credius obtine in justitie anularea creditului, din cauza dobanzii prea mari

- Hotararea judecatoriei prin care Aedificium, fosta Raiffeisen Banca pentru Locuinte, si statul sunt obligati sa achite unui client prima de stat

- Decizia Curtii de Apel Bucuresti in procesul dintre Raiffeisen Banca pentru Locuinte si Curtea de Conturi

- Vodafone, obligata de judecatori sa despagubeasca un abonat caruia a refuzat sa-i repare un telefon stricat sau sa-i dea banii inapoi (decizia instantei)

- Taxa de reziliere a abonamentului Vodafone inainte de termen este ilegala (decizia definitiva a judecatorilor)

Stiri economice

- Producția industrială pe februarie, cu aproape 7% sub cea din urmă cu cinci ani

- Inflația anuală a revenit la nivelul de la finele anului anterior

- Pensia reală de asigurări sociale de stat a crescut anul trecut cu 2,9%

- Producția de cereale boabe pe 2023, cu o zecime mai mare față de anul precedent

- România, țara UE cu cea mai mare creștere a costului salarial

Statistici

- Care este valoarea salariului minim brut si net pe economie in 2024?

- Cat va fi salariul brut si net in Romania in 2024, 2025, 2026 si 2027, conform prognozei oficiale

- România, pe ultimul loc în UE la evoluția productivității muncii în agricultură

- INS: Veniturile romanilor au crescut anul trecut cu 10%. Banii de mancare, redistribuiti cu precadere spre locuinta, transport si haine

- Inflatia anuala - 13,76% in aprilie 2022 si va ramane cu doua cifre pana la mijlocul anului viitor

FNGCIMM

- Programul IMM Invest continua si in 2021

- Garantiile de stat pentru credite acordate de FNGCIMM au crescut cu 185% in 2020

- Programul IMM invest se prelungeste pana in 30 iunie 2021

- Firmele pot obtine credite bancare garantate si subventionate de stat, pe baza facturilor (factoring), prin programul IMM Factor

- Programul IMM Leasing va fi operational in perioada urmatoare, anunta FNGCIMM

Calculator de credite

- ROBOR la 3 luni a scazut cu aproape un punct, dupa masurile luate de BNR; cu cat se reduce rata la credite?

- In ce mall din sectorul 4 pot face o simulare pentru o refinantare?

Noutati BCE

- Acord intre BCE si BNR pentru supravegherea bancilor

- Banca Centrala Europeana (BCE) explica de ce a majorat dobanda la 2%

- BCE creste dobanda la 2%, dupa ce inflatia a ajuns la 10%

- Dobânda pe termen lung a continuat să scadă in septembrie 2022. Ecartul față de Polonia și Cehia, redus semnificativ

- Rata dobanzii pe termen lung pentru Romania, in crestere la 2,96%

Noutati EBA

- Bancile romanesti detin cele mai multe titluri de stat din Europa

- Guidelines on legislative and non-legislative moratoria on loan repayments applied in the light of the COVID-19 crisis

- The EBA reactivates its Guidelines on legislative and non-legislative moratoria

- EBA publishes 2018 EU-wide stress test results

- EBA launches 2018 EU-wide transparency exercise

Noutati FGDB

- Banii din banci sunt garantati, anunta FGDB

- Depozitele bancare garantate de FGDB au crescut cu 13 miliarde lei

- Depozitele bancare garantate de FGDB reprezinta doua treimi din totalul depozitelor din bancile romanesti

- Peste 80% din depozitele bancare sunt garantate

- Depozitele bancare nu intra in campania electorala

CSALB

- La CSALB poti castiga un litigiu cu banca pe care l-ai pierde in instanta

- Negocierile dintre banci si clienti la CSALB, in crestere cu 30%

- Sondaj: dobanda fixa la credite, considerata mai buna decat cea variabila, desi este mai mare

- CSALB: Romanii cu credite caută soluții pentru reducerea ratelor. Cum raspund bancile

- O firma care a facut un schimb valutar gresit s-a inteles cu banca, prin intermediul CSALB

First Bank

- Ce trebuie sa faca cei care au asigurare la credit emisa de Euroins

- First Bank este reprezentanta Eurobank in Romania: ce se intampla cu creditele Bancpost?

- Clientii First Bank pot face plati prin Google Pay

- First Bank anunta rezultatele financiare din prima jumatate a anului 2021

- First Bank are o noua aplicatie de mobile banking

Noutati FMI

- FMI: criza COVID-19 se transforma in criza economica si financiara in 2020, suntem pregatiti cu 1 trilion (o mie de miliarde) de dolari, pentru a ajuta tarile in dificultate; prioritatea sunt ajutoarele financiare pentru familiile si firmele vulnerabile

- FMI cere BNR sa intareasca politica monetara iar Guvernului sa modifice legea pensiilor

- FMI: majorarea salariilor din sectorul public si legea pensiilor ar trebui reevaluate

- IMF statement of the 2018 Article IV Mission to Romania

- Jaewoo Lee, new IMF mission chief for Romania and Bulgaria

Noutati BERD

- Creditele neperformante (npl) - statistici BERD

- BERD este ingrijorata de investigatia autoritatilor din Republica Moldova la Victoria Bank, subsidiara Bancii Transilvania

- BERD dezvaluie cat a platit pe actiunile Piraeus Bank

- ING Bank si BERD finanteaza parcul logistic CTPark Bucharest

- EBRD hails Moldova banking breakthrough

Noutati Federal Reserve

- Federal Reserve anunta noi masuri extinse pentru combaterea crizei COVID-19, care produce pagube "imense" in Statele Unite si in lume

- Federal Reserve urca dobanda la 2,25%

- Federal Reserve decided to maintain the target range for the federal funds rate at 1-1/2 to 1-3/4 percent

- Federal Reserve majoreaza dobanda de referinta pentru dolar la 1,5% - 1,75%

- Federal Reserve issues FOMC statement

Noutati BEI

- BEI a redus cu 31% sprijinul acordat Romaniei in 2018

- Romania implements SME Initiative: EUR 580 m for Romanian businesses

- European Investment Bank (EIB) is lending EUR 20 million to Agricover Credit IFN

Mobile banking

- Comisioanele BRD pentru MyBRD Mobile, MyBRD Net, My BRD SMS

- Termeni si conditii contractuale ale serviciului You BRD

- Recomandari de securitate ale BRD pentru utilizatorii de internet/mobile banking

- CEC Bank - Ghid utilizare token sub forma de card bancar

- Cinci banci permit platile cu telefonul mobil prin Google Pay

Noutati Comisia Europeana

- Avertismentul Comitetului European pentru risc sistemic (CERS) privind vulnerabilitățile din sistemul financiar al Uniunii

- Cele mai mici preturi din Europa sunt in Romania

- State aid: Commission refers Romania to Court for failure to recover illegal aid worth up to €92 million

- Comisia Europeana publica raportul privind progresele inregistrate de Romania in cadrul mecanismului de cooperare si de verificare (MCV)

- Infringements: Commission refers Greece, Ireland and Romania to the Court of Justice for not implementing anti-money laundering rules

Noutati BVB

- BET AeRO, primul indice pentru piata AeRO, la BVB

- Laptaria cu Caimac s-a listat pe piata AeRO a BVB

- Banca Transilvania plateste un dividend brut pe actiune de 0,17 lei din profitul pe 2018

- Obligatiunile Bancii Transilvania se tranzactioneaza la Bursa de Valori Bucuresti

- Obligatiunile Good Pople SA (FRU21) au debutat pe piata AeRO

Institutul National de Statistica

- Comerțul cu amănuntul, în expansiune la început de an

- România, pe locul 2 în UE la creșterea comerțului cu amănuntul în ianuarie 2024

- Comerțul cu amănuntul, în creștere cu 1,9% pe anul 2023

- Comerțul cu amănuntul, în creștere pe final de an

- Comerțul cu amănuntul, stabilizat la +2% față de anul anterior

Informatii utile asigurari

- Data de la care FGA face plati pentru asigurarile RCA Euroins: 17 mai 2023

- Asigurarea împotriva dezastrelor, valabilă și in caz de faliment

- Asiguratii nu au nevoie de documente de confirmare a cutremurului

- Cum functioneaza o asigurare de viata Metropolitan pentru un credit la Banca Transilvania?

- Care sunt documente necesare pentru dosarul de dauna la Cardif?

ING Bank

- La ING se vor putea face plati instant din decembrie 2022

- Cum evitam tentativele de frauda online?

- Clientii ING Bank trebuie sa-si actualizeze aplicatia Home Bank pana in 20 martie

- Obligatiunile Rockcastle, cel mai mare proprietar de centre comerciale din Europa Centrala si de Est, intermediata de ING Bank

- ING Bank transforma departamentul de responsabilitate sociala intr-unul de sustenabilitate

Ultimele Comentarii

-

Refuz de plată la o benzinărie suma de 103 euro

Mi s-au retras de două ori suma de 48 euro și suma de 103 euro suma corectă este de 48 de euro ... detalii

-

nevoia de banci

De ce credeti ca acum nu mai avem nevoie de banci si firme de asigurari? Pentru ca acum avem ... detalii

-

Mda

ACUM nu e nevoie de asa ceva .. acum vreo 20 de ani era nevoie ... ACUM de fapt nu mai e asa multa ... detalii

-

oprire pe salariu garanti bank

mi sa virat 2500de lei din care a fost oprit 850 de lei urmand sa mi se deblocheze restul sumei ... detalii

-

Amânare rate

Buna ziua, Am rămas în urma cu ratele , va rog frumos sa ma ajutați cumva , soțul a pierdut ... detalii