Erste Bank: CEE should do much better than in the post-Lehman period |

Autor: Bancherul.ro

2011-10-17 23:06 |

|

Three years after the Lehman collapse, the financial market is troubled by a new storm. The growing debt overhang of advanced economies and too many unanswered questions about the future model of the Euro Area have increased uncertainty on the markets. ‘’At a first glance, the current situation in CEE might look similar to the post-Lehman period, as the spill-over channels remain the same – the potential collapse of global demand and sudden stop or even reversal of capital flows.

Three years after the Lehman collapse, the financial market is troubled by a new storm. The growing debt overhang of advanced economies and too many unanswered questions about the future model of the Euro Area have increased uncertainty on the markets. ‘’At a first glance, the current situation in CEE might look similar to the post-Lehman period, as the spill-over channels remain the same – the potential collapse of global demand and sudden stop or even reversal of capital flows.

So, if the Euro Area decelerates sharply, Central and Eastern Europe will not avoid contagion. But there are three reasons why CEE should do much better this time (relative to the Euro Area) than in the post-Lehman period: much lower public debt levels, improved fiscal consolidation and trimmed down current account deficits," says Juraj Kotian, Co-Head Macro/Fixed Income Research CEE at Erste Group, cited in a bank press release.

CEE in 2011 versus 2008: three things that have changed

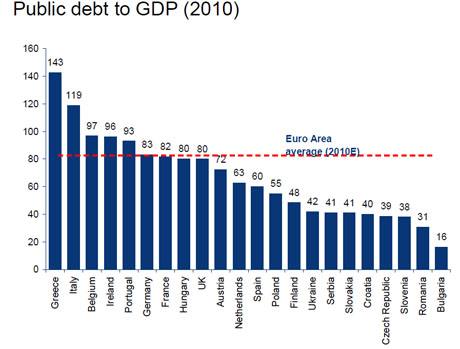

1. The debt level finally matters – CEE countries are far less indebted than Western economies

None of the CEE8 countries is in such a challenging situation in terms of current account imbalances, sustainability of public debt or contingent liabilities in the banking sector like Eurozone peripheral countries. This argument was partially valid also in 2009, when markets were focused on external imbalances of some CEE countries, but at that time markets were completely ignoring the fact that CEE countries are far less indebted than governments or the private sector in the Euro Area. The current situation shows that now markets better differentiate between countries according to their level of debt. For example, Romania and the Czech Republic saw their ratings upgraded as an acknowledgement of their fiscal consolidation progress. Debt levels are rather healthy compared to advanced European economies, which translates into less danger in terms of their growth potential.

2. Structural budget deficits have improved considerably

The fiscal deficits of CEE countries increased during the crisis, but remained well below more problematic Euro Area countries. The widening of fiscal deficits in CEE had its roots in the pre-crisis period, as countries did not sufficiently consolidate their public finances in the boom years. The high growth of cyclically boosted tax revenues had helped to mask the underlying structural deficits, which later showed up in full blow. Almost all CEE countries entered the crisis with a structural deficit above 3% of GDP. In the meantime, governments that were under the strongest market pressure (and under the IMF program) took decisive steps towards fiscal consolidation and brought their structural deficits below pre-crisis levels. The most striking result was achieved in Romania, where the structural deficit has been reduced from almost 9% of GDP in 2007 to about 3.3% of GDP, as estimated by the European Commission for 2011. Hungary made significant progress too, but through either one-off or temporary measures, often with an adverse effect on economic growth. These measures will need to be replaced by genuine reforms and savings in public expenditures.

’’What else has put CEE countries in a much better position compared to the post-Lehman shock? It is their trimmed down current account deficits, the former Achilles Heel of some CEE countries. Romania’s current account deficit sharank from almost 14% to below 5% of GDP, Croatia’s from 7% to 1.4% and Hungary’s turned into a surplus of 2.8%, from a deficit of 7% of GDP in 2007. This has substantially reduced the new external financing needs of CEE countries, which had made them so vulnerable in the past. The progress was achieved much faster than in some peripheral countries,’’ explains Kotian.

3. Cyclical component of GDP is low – magnitude of potential slowdown is small

CEE economies are now in a completely different stage of their economic cycle compared to three years ago, which means the current downturn has a less severe impact upon their economic growth. In 2008, investment and inventories were extremely high and made the economies operate above their potential GDP. Since then, those two cyclical components of GDP have become more moderate. The economies are now operating near or below potential and thus GDP would not contract that strongly in the case of an external shock.

Erste Group analysts further point out that the slowdown has little chance to repeat to such an extent, given that investment rates have already declined sharply - from the pre-crisis peak of 30% of GDP to a more neutral 20% of GDP. Furthermore, CEE economies are running close or even slightly below their potential, compared to an output gap ranging between 1.8% - 10% one year before the Lehman collapse.

The prolonged crisis increased the uncertainty, with immediate consequences for the entire chain of economic decisions, starting with dented consumer sentiment, lower investments in the manufacturing sector and ending with high risk aversion, higher financing costs and a strong preference for cash or other highly liquid assets worldwide. Bottom line, this does not help economic growth, which already decelerated in 2Q. The breakdown of GDP for 2Q published in September revealed that in many CEE countries investments and net exports were the only contributor to GDP growth, while household and government consumption stalled or even contracted.

Due to the gloomy global outlook, Erste Group analysts have recently revised down the forecasts for CEE. Still, the CEE region should outperform the Euro Area growth next year, except for Hungary, where the high legislative uncertainty weighs heavily. The GDP growth of CEE8 economies is to slow down next year to an average 2.6% y/y, from 2.8% y/y expected for this year, based on 0.9% growth of the Euro Area next year with further downside potential.

“It is hard to believe that the damage done by the slow progress in solving the Euro Area debt crisis could be completely reversed. However, if a solution is found that could calm down the markets, this could open the way for some central banks in CEE to proceed with rate cuts. We think that CEE countries are much better prepared to deal with the crisis than they were three years ago. Due to the reduction of fiscal and external imbalances, the economic contraction should not be as severe as in 2009”, concludes Juraj Kotian.

|

|