BERD a publicat ultima editie a monitorului creditelor neperformante din regiunea Centrul si Sud-Estul Europei (NPL monitor for the CESEE region – H2 2023), aferent primei jumatati a anului 2023, in care exista si statistici privind creditele performante pe fiecare tara (vezi foto).

In analizat BERD se precizeaza urmatoarele, cu privire la evolutia creditelor neperformante:

Executive summary

Heightened geopolitical risk, compounded by inflationary pressures and a surge in the cost of living, continues to put strain on the debt-servicing capacity of borrowers.

Banking regulators and supervisors remain vigilant, reiterating their warning of possible deterioration in banks’ asset quality across the European Union (EU) and the broader central, eastern and south-eastern European (CESEE) region.

The banking sector has shown resilience to date, thanks to the comprehensive government support measures put in place to mitigate negative impacts on bank asset quality, as well as prudent and effective banking supervision. However, early – albeit limited – signs of credit stress are starting to emerge across most types of borrower and asset class.

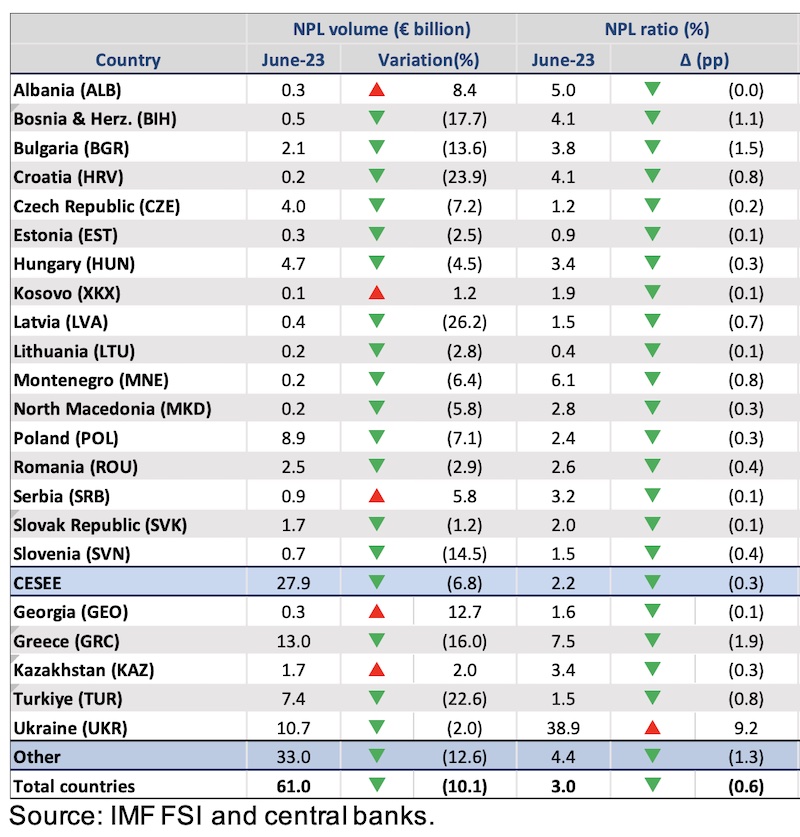

The latest data show that the average share of non-performing loans (NPLs) to total loans in the CESEE region stood at 2.2 per cent as at 30 June 2023, down 0.3 percentage point from the previous year, once again setting a new multi-year low.

The NPL coverage ratio remained stable at 64.3 per cent.

Stage 2 and stage 3 loans, as categorised by the accounting principles of the International Financial Reporting Standards (IFRS) 9, both showed a marginal decrease over the same period. As the European Central Bank (ECB) has said, the recent positive data indicate that banking institutions are well capitalised and have strong liquidity positions compared with past crises, enabling them to maintain low NPL levels despite the challenging macroeconomic landscape.

Nonetheless, the uncertain economic backdrop continues to raise concerns about the medium- term outlook for banks’ asset quality. While inflation and interest-rate hikes have not yet led to a significant decline in asset quality, persistent inflation, rapid monetary policy tightening and geopolitical uncertainties could potentially trigger new shocks, leading to further corrections in asset prices, in turn affecting credit risk and possibly NPLs.

Risk assessments in the EU are now all pointing to a potential decline in asset quality for most large loan segments in the coming year. Rising interest rates and persistent inflation may adversely impact over-leveraged households and companies, hampering their ability to service debt.

A tightening of financial conditions can also be observed, both in terms of the cost of credit and its availability, putting additional strain on already stressed borrowers. Regulators are also warning that the real economic impact of tighter financial conditions has yet to fully materialise, which could exacerbate the pressure on credit risk and NPLs.

Assets most likely to be affected by further shocks include real-estate lending, unsecured consumer lending, assets that have benefited from pandemic-related support measures, and sectors particularly vulnerable to rising inflation and volatile commodity prices. Despite recent corrections in the real-estate market, the sector remains subject to further risk of a downturn as interest rates affect both asset valuations and affordability for borrowers.

In this context, it is crucial for regulators and banking supervisors to further assess banks´ readiness to manage any increase in distressed debt and refinancing challenges. They need to remain vigilant for any signs of deteriorating asset quality or a rise in NPLs within the financial sector. It is of utmost importance for supervisors to continue preparing for potential economic downturns and emphasise the necessity of robust valuation, modelling and risk management practices.

Furthermore, banks also need to be fully prepared for potential declines in asset quality. This includes ensuring that they have robust credit risk monitoring and management, appropriate loan classification, accurate loan staging and adequate loan loss provisioning.

NPL volumes decreased 6.8 per cent in the 12 months to June 2023

• At a regional level, NPL volumes fell 6.8 per cent to €27.9 billion in the 12 months from 30 June 2022 to 30 June 2023.3

• In relative terms, the decline in NPL stocks was most significant in Latvia, Croatia and Bosnia and Herzegovina, where they fell 26.2 per cent, 23.9 per cent and 17.7 per cent, respectively.

• In absolute terms, the largest contributor to the decline was Poland, where the stock of NPLs

declined by €0.7 billion, or 7.1 per cent.

• Only three economies saw an increase in NPL volumes: Albania (8.4 per cent), Serbia (5.8 per

cent) and Kosovo (1.2 per cent).

• While some of this decrease in NPL volumes can be attributable to NPL sales from banks to

third-party investors, this is expected to account only for a fraction of the reduction, as the level of publicly reported transactions remained subdued during the period. Loans write-offs and progress on restructuring, enforcement and recovery efforts are expected to have played a key role.

The average NPL ratio across the CESEE region declined slightly once again in year to June 2023, reaching its lowest level in recent years

• The average regional NPL ratio (the proportion of NPLs to total gross loans) decreased 0.3 percentage point to 2.2 per cent over the 12-month period to 30 June 2023. Once again, this set a record low since the NPL Monitor was first published in 2016.

• Bulgaria saw the largest decline during the year, with a 1.5 percentage-point drop to 3.8 per cent.

• None of the countries experienced an increase in the NPL ratio during this period.