Guidelines on legislative and non-legislative moratoria on loan repayments applied in the light of the COVID-19 crisis – Consolidated version updated on 2 December 2020

1. Executive summary

The outbreak of the COVID-19 pandemic and the response measures that have been adopted in many countries across the globe and in the European Union (EU), including various forms of population confinement, have significant economic consequences.

In particular, many businesses and private individuals affected by the crisis may face liquidity shortages and difficulties in timely payment of their financial and other commitments. This could in turn have an impact on credit institutions, as delays in the repayment of credit obligations lead to a larger number of defaults and increased own funds requirements for credit institutions.

In these circumstances, in order to minimise the medium- and long-term economic impacts of the efforts taken to contain the COVID-19 pandemic, Member States have implemented a broad range of support measures.

These measures include, in many instances, some forms of moratorium on payments of credit obligations, with the aim of supporting the short-term operational and liquidity challenges faced by borrowers.

As these moratoria in practice are adopted in various forms across jurisdictions, clarification is necessary on the application of the definition of default and classification of forbearance in the context of these various measures.

The European Banking Authority (EBA) clarified a number of aspects in relation to the use of public and private payment moratoria (i.e. the legislative and non-legislative proposalsreferred to in these guidelines) in its statement of 25 March2020.

It also, however, noted that further detailed guidance was necessary to ensure consistent application. Consequently, these guidelines aim to provide clarity on the treatment of legislative and non-legislative moratoria applied before 31 March 2021.

These guidelines clarify which legislative and non-legislative moratoria do not to trigger forbearance classification, while in all other cases the assessment must be done on a case-by case

basis. Furthermore, these guidelines supplement the EBA Guidelines on the application of the definition of default as regards the treatment of distressed restructuring.

In particular, these guidelines clarify that the payment moratoria do not trigger forbearance classification and the

assessment of distressed restructuring if they are based on the applicable national law or on an industry- or sector-wide private initiative agreed and applied broadly by relevant credit institutions.

While the EBA is supportive of the measures and initiatives taken in the Member States in order to address the economic consequences of the COVID-19 pandemic, it is also aware of the need to ensure that the risk is identified and measured in a true and accurate manner.

Therefore, institutions must continue to adequately identify those situations where obligors may face longerterm financial difficulties and classify them in accordance with the existing regulation. This is crucial to provide true information about the quality of banks’ portfolios to market participants, and to

ensure that institutions are adequately capitalised.

The requirements of the remaining framework therefore continue to be in place, which is especially relevant in the light of the fact that EU and national authorities have also taken steps to release capital buffers and similar measures on the

basis of the existing risk metrics.

In order to allow effective monitoring of the effects of the COVID-19 pandemic and the application of response measures, it is necessary for institutions to collect information about the scope and effects of the use of the moratoria.

Institutions are expected to make use of the general payment

moratoria in a transparent manner, providing relevant information to their competent authorities, while specific disclosure requirements to the public will be published at a later point in time.

Due to the urgency of the matter and the specific focus of these guidelines on COVID-19 pandemicrelated measures, the EBA decided not to carry out public consultations or a cost-benefit analysis in this case.

The EBA has notified the Banking Stakeholder Group (BSG) of its intention to issue the guidelines but has not requested the BSG’s advice.

2. Background and rationale

Introduction

The outbreak of the COVID-19 pandemic and the pandemic response measures that have been adopted in many countries across the globe and within the EU, including various forms of

population confinement, have significant economic consequences.

In particular, many businesses, especially small and medium enterprises (SMEs), and private individuals affected by

the crisis may face liquidity shortages and difficulties in timely payment of their financial and other commitments.

This could in turn have an impact on credit institutions, as delays in the repayment of credit obligations lead to a larger number of defaults and increased own funds requirements for credit institutions.

These concerns resurfaced in light of the second COVID-19

outbreak and the accompanied government restrictions taken in many EU countries, whereby many businesses and private individuals continue to be severely affected by the crisis.

In these circumstances, in order to minimise the medium- and long-term economic impacts of the efforts taken to contain the COVID-19 pandemic, Member States have implemented a broad range of support measures.

These measures include, in many instances, some forms of

moratorium on payments of credit obligations, with the aim of supporting the operational and liquidity challenges faced by borrowers.

As these moratoria in practice are adopted in various forms across jurisdictions (some Member States have introduced jurisdiction-wide moratoria based on specific legislation, whereas in many others moratoria have been implemented

through voluntary industry-wide or individual initiatives by institutions, or combination thereof), this raises questions of the legal effect they have on the current prudential framework,

especially in the context of the application of the definition of default and classification of forbearance.

These guidelines aim to clarify the following points in the context of the COVID-19 pandemic: (i) the criteria that payment moratoria have to fulfil not to trigger forbearance classification, (ii) the application of the prudential requirements in the context of these moratoria and (iii) ensuring the consistent treatment of such measures in the calculation of own funds requirements.

While the payment moratoria to mitigate the financial impacts of the COVID-19 pandemic are taking different forms in different Member States, they tend to have similar objectives and similar economic substance.

In this context, it is important to ensure that the treatment of various non-legislative initiatives is consistent with the moratoria applied through the legislation, if they have the same economic substance.

Some private initiatives may take the form of industry-wide measures, agreed and documented by institutions through their industry associations in a given jurisdiction. In some Member

States, such initiatives are openly encouraged by the government, sometimes supplemented by government guarantees, which may provide further incentives for institutions to adopt these measures.

In other cases, individual institutions or groups of institutions have offered similar payment holidays to their affected obligors, but there is no coordination or agreement with all institutions to apply the measures across the sector.

The common element of all of these measures is that they all provide for a payment relief for obligors affected by the COVID-19 pandemic by allowing suspension or postponement of payments within a specified period of time, allowing the obligors to return to regular payments after the situation is back to normal.

The EBA is supportive of the measures and initiatives taken in the Member States to address the economic consequences of the COVID-19 pandemic. The EBA sees the payment moratoria as effective tools to address short-term liquidity difficulties caused by the limited or suspended operation of many businesses and individuals. However, it must also be stressed that, especially in difficult economic circumstances, it is particularly important to ensure that risk is identified

and measured in a true and accurate manner.

Institutions must therefore continue to adequately identify those situations where short-term payment challenges may transpose into long-term financial difficulties and eventually lead to insolvency.

These cases should be correctly identified and classified in accordance with the existing requirements to ensure that financial statements present true information about the

quality of banks’ portfolios to market participants and that institutions are adequately capitalised.

Furthermore, the real impact of the economic shock can only be assessed based on adequate and consistent classification and measurement of risk. Consequently, institutions should continue to apply the prudential definitions in a consistent manner.

In order to ensure consistency among the measures taken, these guidelines provide clarifications on how to apply

the definition of default in accordance with Article 178 of Regulation (EU) No 575/2013 as regards the specific situation of the application of general payment moratoria.

Due to the urgency of the matter and the specific focus of these guidelines on COVID-19 pandemic-related measures, the EBA decided not to carry out public consultations or a costbenefit analysis in this case.

The EBA has notified the BSG of its intention to issue the guidelines but has not requested the BSG’s advice.

The clarifications provided are in line with Article 178 of Regulation (EU) No 575/2013, with Commission Delegated Regulation (EU) 2018/171 on the materiality threshold for credit obligations past due and with the EBA Guidelines on the application of the definition of default under Article 178 of Regulation (EU) No 575/2013.

Classification of exposures under the definition of forbearance and distressed restructuring

In the current regulatory framework1, ‘forbearance’ means that credit institutions grant a concession (e.g. temporarily postpone capital and/or interest payments of a loan) when they identify that a borrower is experiencing or is likely to experience financial difficulty in repaying a loan(s).

Credit institutions grant measures specific to the financial circumstances of the borrower and the loan agreement, with the aim of helping the borrower who is experiencing

temporary difficulties with the repayment obligations.

It is clarified in these guidelines that the application of a general payment moratorium that meets the requirements of these guidelines would not in itself lead to a reclassification under the definition of forbearance.

However, institutions should continue to categorise the exposures as performing or non-performing in accordance with the applicable requirements.

More precisely, as a general principle, before granting a forbearance measure, credit institutions should carry out an individual assessment of the repayment capacity of the borrower and grant forbearance measures tailored to the specific circumstances of the borrower in question2.

The legislative and non-legislative moratoria schemes introduced in response to the COVID-19 pandemic have a generally preventative nature and are not borrower specific, as they aim to address systemic risks that may occur in the wider EU economy in the future.

Consequently, these guidelines provide the criteria that general payment moratoria have to fulfil to be considered not meeting the definition of forbearance. It has to be noted, however, that, where exposures have already been subject to forbearance measures before the application of such moratoria, this classification should not be changed.

Furthermore, it is specified in paragraph 49 of the EBA Guidelines on the application of the definition of default that, where forbearance measures were extended towards the borrower, this should be considered distressed restructuring, which, in accordance with Article 178(3)(d) of Regulation (EU) No 575/2013, is an indication of unlikeliness to pay if it leads to diminished financial obligation.

Given that the application of a general moratorium is not a forbearance measure, it should also not be considered distressed restructuring and the consideration of diminished financial obligation is not applicable.

It should also be noted, however, that where institutions do not apply any general payment moratoria as specified in these guidelines, but instead apply some form of individual measures

and renegotiate the loans taking into account the specific situation of individual obligors, they have to assess whether such individual measures meet the definition of forbearance in accordance with Article 47b of Regulation (EU) No 575/2013, as amended by Regulation (EU) 2019/630.

Also in such cases, there is no automatic reclassification of the exposures, but this would be based on individual assessment. Measures classified as forbearance should be considered to constitute distressed restructuring in accordance with Article 178(3)(d) of that regulation.

In such cases, to decide whether the obligor should be classified as defaulted, institutions are required to assess whether these measures led to diminished financial obligation, as further clarified in paragraphs 50 to 52 of the EBA Guidelines on the application of the definition of default.

Conditions for the general payment moratoria

In order to ensure that the definition of forbearance continues to be applied in an appropriate and consistent manner, these guidelines specify conditions that the general legislative and nonlegislative moratoria have to fulfil in order not to be considered forbearance. These conditions include, in particular, the following.

The moratorium was launched in response to the COVID-19 pandemic. The scope and time of application of these guidelines are limited and they apply only to specific measures taken in

response to the current economic situation caused by the COVID-19 pandemic.

In order to ensure this limited scope, it is required that the moratorium in question is announced and applied before 31 March 20213.

This means that the guidelines apply also to moratoria launched

before the application of these guidelines.

The moratorium has to be broadly applied. This condition aims to ensure that the proposed treatment applies to the moratoria that are similar in economic substance, regardless of whether they are legislative or non-legislative.

Given that legislative moratoria apply to all institutions within a given jurisdiction, a similarly broad scope of application also has to be ensured for the non-legislative moratoria.

However, the EBA is aware that different structures and organisations of the banking industry exist in different countries; therefore, this condition has to be specified in a sufficiently flexible manner.

While it may not be possible to encompass all credit institutions within a given Member State with a single non-legislative moratorium, institutions are encouraged to make an effort to coordinate actions to the extent possible.

In this context, it has to be noted that coordination may be achieved in various manners. Where there are banking associations made up of significant numbers of institutions or of institutions in a specific segment of the banking sector within a given country, the moratorium scheme may be coordinated by such associations.

Where such associations do not exist, the measures may be coordinated in a more ad hoc manner between peer institutions.

The EBA acknowledges that several non-legislative moratoria may exist in a single country and that non-legislative moratoria may exist alongside legislative moratoria. However, for the

change of the schedule of payment due to the application of the moratorium not to be considered forbearance, the moratorium has to be based on a sufficiently broad initiative.

For this purpose, an initiative of a single institution is not considered sufficiently broad, as it would therefore be a tailor-made solution. In such a case, the institution would have to analyse the exposures subject to the moratorium and apply the definition of forbearance on a case-by-case basis.

The moratorium has to apply to a broad range of obligors. This condition is necessary to ensure that the change of the schedule of payment does not address specific financial difficulties of specific obligors, as this would meet the definition of forbearance.

Therefore, in order to benefit from the treatment specified in these guidelines, the moratorium has to be available to a large,

predefined group of obligors, regardless of the assessment of their creditworthiness.

As the moratorium is supposed to address systemic short-term liquidity shortages, the selection criteria have to be sufficiently broad. Examples of such broad criteria include, but are not limited to, a specific exposure class or sub-exposure class (e.g. retail, private individuals, SMEs or corporates), a specific product range (e.g. mortgage loans) or obligors from specific regions or certain industry sectors that are most affected by the crises caused by the COVID-19 pandemic.

For the purpose of the application of these guidelines, the moratorium cannot apply to obligors based on their creditworthiness. For instance, it is not acceptable for the moratorium to apply only to obligors included on a watch list or those clients who experienced financial difficulties

before the outbreak of the COVID-19 pandemic, as this would clearly lead to forbearance classification.

By contrast, it is possible for the scope of application of the moratorium to be limited to performing obligors who did not experience any payment difficulties before the application of the moratorium. However, where the moratorium applies to exposures that were already classified as forborne or defaulted at the moment of the application of the moratorium, this classification must be maintained.

Furthermore, it is clarified that the application of the moratorium is not obligatory for the obligors. In particular, it may be based on an application from the obligor requesting the

application of the moratorium and presenting the extent to which the obligor is affected by the COVID-19 pandemic.

In this case, the moratorium can be considered general in accordance with these guidelines if the assessment of the application does not involve the assessment of the creditworthiness or payment capacity of the obligor and the conditions of the moratorium are standardised and available to all obligors affected by the COVID-19 pandemic.

Examples of such conditions include the change of employment status in the case of private individuals or the need close operations for a given period of time in the case of SMEs.

Furthermore, as explained above, in this case, the obligors must apply and the decision on the application of the

moratorium must be taken before 31 March 2021.

The same moratorium offers the same conditions. While the same conditions have to apply or be offered to all clients subject to the moratorium, it is also possible that different moratoria apply to different segments of exposures or obligors. However, in any case, it has to be ensured that the moratorium applies broadly and to a large number of obligors of an institution.

For instance, different moratoria with different conditions may apply to private individuals and to SMEs. Similarly, a separate moratorium could be launched for a specific range of products, for instance mortgage loans.

This gives institutions the possibility of participating in different

moratoria, depending on their business model. For each of such moratoria, an institution may apply the provisions provided in these guidelines where the moratorium applies to all exposures

of that institution within the scope of moratorium.

The moratorium changes only the schedule of payments. This condition is consistent with the objective of the moratorium to address the systemic short-term liquidity shortages. In order to

achieve this objective, the moratoria suspend, postpone or reduce the payments (principal, interest or both) within a limited period of time.

This clearly affects the whole schedule of payment and may lead to increased payments after the period of the moratorium or an extended duration of the loan. However, the moratorium should not affect other conditions of the loan, in particular the interest rate, unless such change only serves for compensation to avoid losses which an institution otherwise would have due to the delayed payment schedule under the moratorium, which would allow the impact on the net present value to be neutralised.

Otherwise, this would be a specific solution for individual loans and could lead to a significant change in the net present value of the credit obligation and in such a case, a forbearance classification would have to be considered. In this context, in the case of contracts based on variable interest rate, the usual adaptation of the interest rate based on the changes of the

benchmark rate is not considered a change to the terms and conditions of the loan.

Furthermore, the EBA is aware that some general payment moratoria are accompanied by the public guarantees offered in the response to the COVID-19 pandemic. The application of such guarantee associated to the moratorium is not considered to change the terms and conditions of the loan, regardless the way these guarantees are treated under the applicable accounting framework.

The moratorium does not apply to new loans granted after the launch of the moratorium. It has to be ensured that the moratorium addresses a specific issue arising as a result of the

COVID-19 pandemic and is not used for new lending granted after the outbreak.

In this context, the use of existing credit lines or renewal of revolving loans is not considered a new loan.

Moreover, in order to establish whether a loan has been granted after the date when the moratorium was announced, and therefore whether it should be considered new for the purposes of the guidelines, it is important to clarify how to evaluate whether a moratorium is new or just a modification of an existing one. In particular, a moratorium should only be

considered new if it covers a new scope of exposures not considered by a previous moratorium.

If a moratorium has a different set of conditions but applies to a similar set of exposures to a previous moratorium, this should be treated as a modification of the existing moratorium. In

this case, the original date on which the moratorium was launched should be used to decide on the treatment of the loan for the purposes of the guidelines (i.e. whether it should be considered a “new” loan or not).

It has to be stressed that institutions are allowed and encouraged to grant new lending to both new and existing clients during the application of the moratorium. However, it is expected that this new lending will follow the normal credit policies and will be based on the assessment of the creditworthiness of the clients, and will take into account any possible associated public guarantees.

These new loans should be adequately structured taking into account the current payment capacities and hence the application of the moratorium should not be necessary. While

granting a new loan to an obligor under the moratorium does not automatically lead to forbearance classification, the individual conditions should be assessed on a case-by-case basis.

Criteria for exposures subject to moratoria 4

EBA however also recognises that the longer is the duration of the payment postponement, suspension or reduction towards the same obligor, the higher is the risk that the obligor is in

fact facing insolvency challenges.

What started, in fact, as a liquidity shortage may have developed into insolvency issues, and could, in the medium term, affect a bank’s capital position and overall stability. In general, this is also the reason why the prudential framework takes a prudent approach to the recognition of these risks.

Nonetheless, in the current situation, the temporary lockdowns of the EU economy, in various degrees, do cause an exceptional set of circumstances, which should be duly recognised.

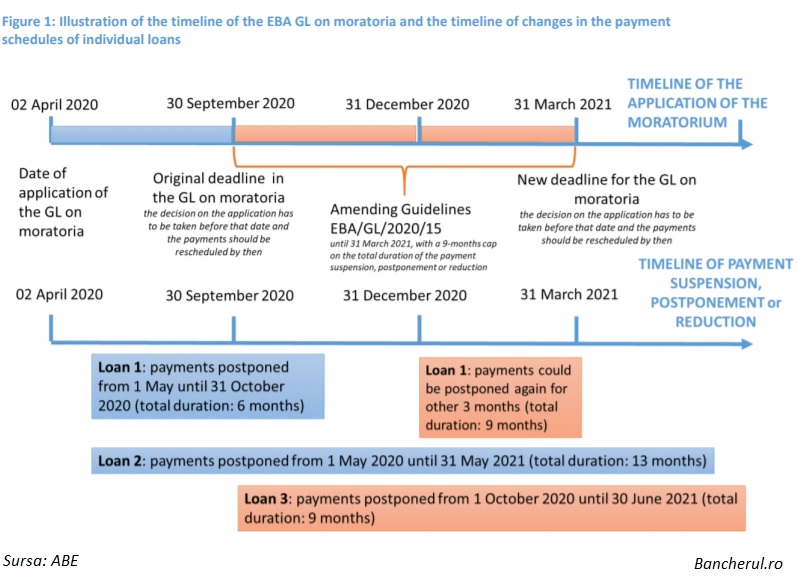

In order to mitigate the risk faced by banks, a constraint has been introduced at the level of each single exposure on the overall length of the payment extension. In particular, the period of time for which payments on a certain loan can be suspended, postponed or reduced as a result of the application (and reapplication) of general payment moratoria should not exceed an overall length of 9 months.

Figure 1 illustrates the relationship between the timeline of the GL on moratoria and the timeline of changes in payment schedules (i.e. limited periods of time by which payments of

principal amounts, interest or full instalments can be suspended, postponed or reduced) agreed by obligors and credit institutions.

The first timeline relates to the deadline for the application of the moratorium scheme of 31 March 2021, whereas the second timeline shows for fictive examples the potential periods during which payments may be postponed, suspended or reduced which are constrained to a total of 9 months.

For a loan contract where a payment suspension of 6 months has already been granted under a general payment moratorium, credit institutions may agree to a further payment suspension of not more than 3 months under a general payment moratorium in accordance with these guidelines.

This is the case for loan 1 shown in Figure 1. Where a payment suspension meets this condition, institutions will not have to reclassify the exposure as forborne or treat it as distressed restructuring, as a result of the application of a general payment moratorium.

This condition ensures that the overall agreed payment extension does not exceed 9 months. This constraint should ensure that the GL on moratoria will allow banks to alleviate the short-term liquidity challenges of their borrowers while reducing the risk of unidentified issues with obligors’ (longterm) insolvency.

Changes in the payment schedules agreed on loan contracts before 30 September 2020 are not subject to this constrained length of 9 months and, therefore, it may be that some already

agreed payment extensions exceed the 9-month cap.

In this respect, the guidelines clarify that these changes in payment schedules, agreed prior to 30 September 2020, are not affected by the 9-month cap requirement.

This implies that, as illustrated in Figure 1, if on 1 May 2020 payments on loan 2 have been suspended for 13 months until 31 May 2021, it would benefit from the treatment of the Guidelines for the full 13 months.

Assessment of unlikeliness to pay

Even where the general payment moratoria are not classified as forbearance measures, this does not remove the obligations for institutions to carefully assess the credit quality of exposures benefiting from these measures and identify any situations in which borrowers are unlikely to pay for the purpose of the definition of default.

These guidelines clarify that institutions should continue to apply their normal policies for the regular reviews of indications of unlikeliness to pay. It is expected that institutions will apply these policies in a risk-based manner, paying particular attention to and prioritising the assessment of those obligors who are most likely to experience payment difficulties.

The EBA acknowledges that the policies and practices with regard to the assessment of unlikeliness to pay may differ depending on the portfolio and the type of obligor, taking into

account the availability of information. In particular, in the case of retail exposures, institutions often apply a regular automatic verification of certain indications of unlikeliness to pay, where

identification of such an indication may lead to either automatic default classification or further, manual, verification.

It is expected that such verifications will continue throughout the duration of the moratorium and after it ends.

Similarly, especially in the case of corporate clients, where potential unlikeliness to pay is assessed manually as part of the regular monitoring process, based on the obligors’ financial

statements and other information, these processes should continue during the application of the moratorium and after it ends.

It is expected that these processes be implemented in a riskbased manner, as, in accordance with paragraphs 106 to 108 of the EBA Guidelines on the application of the definition of default, institutions should have effective processes allowing

them to obtain relevant information and identify defaults in a timely manner.

In the specific context of the COVID-19 pandemic, taking into account the availability of relevant information, institutions should, to the extent possible, prioritise the assessment of cases where it is most likely that the short-term shock may transform into long-term financial difficulties and eventually lead to insolvency.

The guidelines further clarify that, if the schedule of payment has been revised due to the application of the moratorium, the assessment of unlikeliness to pay should be based on the revised schedule.

In addition, institutions should take into account any factors influencing the creditworthiness of the obligor, including any specific support measures adopted in response to the COVID-19 pandemic and available directly to the obligor.

However, the existence of any credit risk mitigation should not exempt the institution from performing the assessment of the

obligor’s unlikeliness to pay or affect the results of such an analysis.

This applies in particular to any guarantees (including public guarantees offered in response to the COVID-19 pandemic), if these are provided for the institutions as credit risk mitigation.

In such cases, while the guarantee may limit the losses for the institution in the event of default of the obligor, it does not affect the payment capabilities of the obligor and hence it should not be taken into account in the assessment of the obligor’s unlikeliness to pay.

Documentation and notifications

It is considered necessary that institutions collect information about the scope and effects of use of the moratoria. This information should be shared with their competent authorities in order to allow effective monitoring of the effects of the COVID-19 pandemic and of the application of response measures.

Furthermore, in order to allow pan-European coordination

and an overview of the use and effects of general payment moratoria in the EU, these guidelines propose that national competent authorities should notify the EBA about the use of any such moratoria in their jurisdiction.

With regard to the scope of the necessary information, it is specified that institutions should clearly identify all obligors and exposures subject to the moratorium (i.e. those within the scope and those where the moratorium was actually applied).

It has to be noted that, due to the noncompulsory character of the moratorium, the number of obligors to whom the moratorium was offered may be larger than the number of obligors to whom it was actually applied.

In particular, where the application of the moratorium requires an application from the obligor, institutions should identify all obligors who may submit such an application. Furthermore, institutions should identify potential economic losses that they may experience because of the application of the moratorium and that may have an impact on their financial statements, including through additional impairment charges.

Finally, institutions are requested to notify to the relevant competent authority or authorities their plans for assessing borrowers’ unlikeness to pay in relation to the exposures subject to (legislative or non-legislative) general payment moratoria 5.

This plan should contain, in particular, information on the process for the assessment of potential unlikeliness to pay, the

sources of information feeding into it and responsibilities in the context of the assessment. This information should allow supervisors to assess the robustness of the institutions processes for the assessment of unlikeness to pay to the current crisis.

In this protracted crisis, in fact, an appropriate unlikeliness to pay assessment acts as a crucial safeguard, since it should ensure the identification of obligors under a moratorium that have long term solvency issues. It is therefore of great importance that banks recognise solvency issues, including in relation to loans subject to payment moratoria.

It is expected that institutions will make use of general payment moratoria in a transparent manner under the current market and regulatory conditions. To this end, the EBA has identified the necessary short-term supervisory reporting and disclosure requirements to monitor the implementation of the measures introduced against COVID-19 and loans that fall under the scope of these guidelines, cognisant of the need for proportionality and efficiency in the current circumstances.

These specific requirements on public disclosures and reporting have been clarified in the Guidelines on reporting and disclosure of exposures subject to measures applied in response to the COVID-19 crisis. 6.

The EBA will continue to monitor the situation closely and aim to provide transparency to the public on the use of moratoria and coverage of public guarantees.7

Furthermore, the EBA will continue to ensure that any lack of clarity on the application of the guidelines is addressed, which has already been done in the EBA Report on the implementation of select COVID-19 policies.8

This report already contains several clarifications, in the form of FAQs, on the implementation of the guidelines, and it also clarifies issues related to the EBA COVID-19 reporting framework and other aspects.

Classification of exposures for the period between 1 October 2020 and 1 December 2020

Finally, transitional arrangements have been specified for changes in the schedule of payments agreed between 1 October and the 1 December 2020. In fact, as shown in Figure 1, the deadline originally set in these Guidelines for the application of the moratorium was 30 September 2020

and this has been extended to 31 March 2021 by the Guidelines amending Guidelines EBA/GL/2020/02 (EBA/GL/2020/15) on 2 December 2020.

The Guidelines, therefore, clarify that where an exposure has been classified as defaulted due to distressed restructuring and/or forborne between 1 October 2020 and 1 December 2020, on the basis of a moratorium that otherwise (i.e. were it not for the date of application being after the original deadline of 30 September 2020) would have met the conditions of the GLs on moratoria prevailing at that time (with deadline of 30 September), this classification can be revisited and potentially reversed in accordance with the treatment set out in these Guidelines. However, the 9-month cap requirement applies to changes in the payment schedule agreed in relation to such exposures.

In Figure 1 above, loan 3 illustrates a situation where the revised payment schedule between the obligor and the bank was agreed after 30 September and, therefore, was not eligible for the treatment set out under the GL on moratoria prevailing at that time (i.e. with deadline of 30 September).

If all the conditions of these Guidelines are met, the treatment set out in these Guidelines can be applied to this exposure, thereby revising its earlier classification.

1

See (i) paragraph 1 of Article 47b of Regulation (EU) 575/2013 introduced by Regulation (EU) 2019/630 of the European Parliament and of the Council of 17 April 2019 amending Regulation (EU) No 575/2013 as regards minimum loss coverage for non-performing exposures and (ii) paragraphs 240 and 241 of Annex V of Commission Implementing Regulation (EU) No 280/2014.

2

See paragraph 140 of the EBA Guidelines on management of non-performing and forborne exposures (EBA/GL/2018/06).

3

The deadline to apply the moratorium was originally 30 June 2020. With the unfolding of the COVID-19 pandemic, in

June 2020, the EBA extended the application date of its guidelines by three months, from 30 June to 30 September 2020, and on the 21 September, communicated its phasing-out. After closely monitoring the developments of the COVID-19

pandemic and, in particular, the impact of the second COVID-19 wave and the relative government restrictions taken in

many EU countries, the EBA has decided to re-activate its guidelines. In particular, the Guidelines amending Guidelines

EBA/GL/2020/02 (EBA/GL/2020/15) have extended the deadline to apply the moratorium to 31 March 2021 and have

introduced two additional safeguards. These are the 9-month cap requirement on the overall length of the payment

holiday and the requirement for institutions to document their plans for the assessment of unlikeliness to pay of obligors

subject to a general payment moratorium.

4

These section on criteria for exposures subject to moratoria has been added as a result of the criteria introduced in the

Guidelines amending Guidelines EBA/GL/2020/02 (EBA/GL/2020/15).

5

This documentation requirement has been introduced by the Guidelines amending Guidelines EBA/GL/2020/02

(EBA/GL/2020/15)

6

See https://eba.europa.eu/regulation-and-policy/supervisory-reporting/guidelines-covid-19-measures-reporting-anddisclosure.

7

A first assessment of this use was published by the EBA on 20 November 2020 (https://eba.europa.eu/banks-reportsignificant-use-covid-19-moratoria-and-public-guarantees).