Fondul Monetar International (FMI) avertizeaza ca bancile romanesti detin prea multe titluri de stat, astfel ca Banca Nationala a Romaniei (BNR) trebuie sa le ceara rezerve suplimentare de capital, in vederea contracararii potentialelor riscuri.

FMI precizeaza in raportul de tara publicat ieri (vezi detalii mai jos) ca este vorba de introducerea unui amortizor (buffer) de risc sistemic, care trebuie atent calibrat, cu scopul de a spori rezistenta sectorului bancar fata de expunerea ridicata la titlurile suverane.

Valoarea titlurilor de stat detinute de sectorul bancar s-a ridicat la aproape 20% din valoarea activelor in 2018, adica in jur de 90 miliarde lei, una dintre cele mai ridicate din Europa, precizeaza FMI.

Iar exceptarea titlurilor de stat de la taxa pe active ar putea stimula bancile sa-si majoreze expunerea, avertizeaza FMI.

FMI critica si noul program Prima Casa, care a devenit mai atragator, in loc sa fie redus progresiv, cum a recomandat.

In privinta taxei pe active, FMI spune ca aceasta ar putea determina majorarea costului creditarii pentru sectorul privat, iar ajustarea taxei in functie de tinte de performanta, precum cresterea creditarii si reducerea marjei de dobanda, ar putea determina distorsiuni in alocarea creditului si resurselor.

FMI vrea sa spuna ca taxa pe active ar putea stimula creditarea mai facila, precum cea pentru populatie, in detrimentul finantarii firmelor, precum si investitiile in titluri de stat.

Incertitudinile create de taxa pe active, precum si introducerea indicelui IRCC, in locul ROBOR, ar putea afecta dezvoltarea sectorului financiar, mai atrage atentia FMI.

FMI cere dobanzi mai mari si consolidare fiscala

In privinta economiei, FMI apreciaza cresterea economica ridicata a Romanei si rata redusa a somajului, dar se arata ingrijorata de cresterea deficitelor gemene (bugetar si de cont curent), rabufnirea inflatiei si stagnarea reformelor structurale si a investitiilor.

Pentru corectarea dezechilibrelor in crestere, FMI recomanda Guvernului trecerea de la o politica fiscala prociclica la una anticiclica, printr-o consolidare fiscala, insotita de o politica monetara mai restrictiva si un curs de schimb mai flexibil, cu alte cuvinte dobanzi mai mari si o depreciere mai mare a leului.

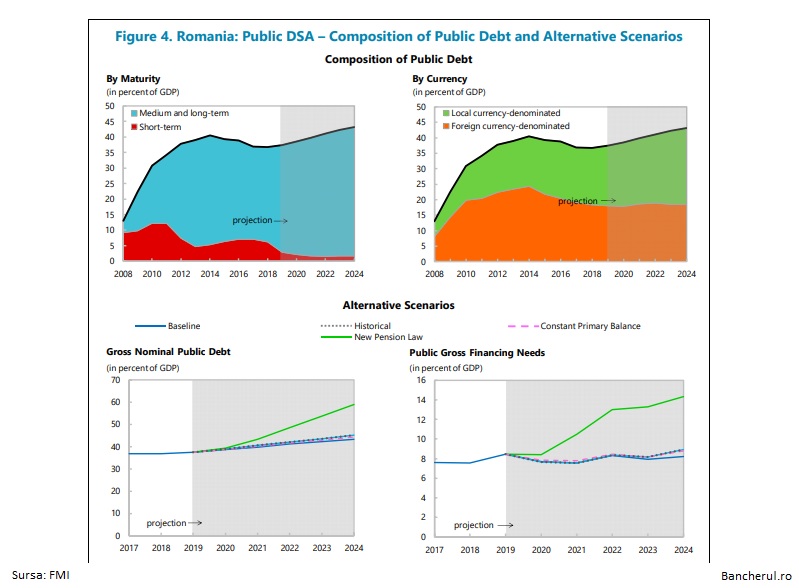

De asemenea, Guvernul este sfatuit sa schimbe noua lege a pensiilor (vezi aici detalii).

IMF Executive Board Concludes Article IV Consultation with Romania (IMF statement)

On August 28, 2019 the Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation (1) with Romania.

Economic growth in Romania was strong in 2018, reflecting pro-cyclical fiscal policy and rapid wage increases. Unemployment reached record lows and financial sector is stable.

Fiscal and current account deficits have been widening in the past few years, reaching respectively 2.8 and 4.5 percent of GDP in 2018.

Although the National Bank of Romania’s (NBR) inflation target was met in 2018, inflation is gathering pace, with headline inflation exceeding the target band since February 2019.

Structural reform agenda remains stalled and investment growth lagged the broader economic activity.

Growth in 2019 is expected to stay above potential at 4 percent, led by continued fiscal stimulus and strong wage growth, and be accompanied by further widening of current account and fiscal deficits. Inflation in 2019 is expected to stay above the NBR’s target band.

Growth is expected to moderate to 3 percent in the medium term as the transitory effects of the fiscal stimulus fade. Lack of progress on structural reforms and subdued investment will constrain potential growth over the medium term.

With macroeconomic imbalances becoming increasingly evident, eroding buffers and undermining Romania’s capacity to withstand adverse shocks, there is a risk that the income convergence with the EU could suffer a setback.

The key domestic risk is an increase in vulnerability caused by policy shocks, including further fiscal stimulus or regresses on structural reforms.

Externally, the key risk stems from a sharper-than-expected external slowdown, which would widen the current account deficit, magnifying financing pressures.

While Romania’s moderate public debt and reserves can provide a temporary cushion, these buffers can prove insufficient under an adverse event.

Executive Board Assessment (2)

Executive Directors agreed with the thrust of the staff appraisal.

They welcomed the strong economic growth and low unemployment, but raised concerns about widening current

account and fiscal deficits and renewed inflation, as well as lagging structural reforms and investment.

To address the growing imbalances, Directors called for shifting from procyclical to countercyclical fiscal policy, complemented by a tighter monetary policy stance and greater exchange rate flexibility.

They further supported strengthening policy predictability and renewing structural reform initiatives to sustain convergence to average EU income levels.

Directors called for a durable fiscal consolidation to help curb the twin deficits and reduce the burden on monetary policy.

They encouraged sustained fiscal reforms to achieve

consolidation over the medium term and improve budget composition.

Directors supported meeting this year’s budget target with quality measures, including shifting expenditures away

from rigid spending–such as wages and pensions–towards investment, reversing the trend of declining public investment in recent years.

They cautioned that the new pension law could undermine fiscal sustainability and should be subjected to a comprehensive review, balancing social, equity and investment needs in line with available fiscal space.

Directors also encouraged modernizing revenue administration by upgrading IT systems and improving compliance risk management, and improving expenditure efficiency and transparency through stronger expenditure reviews and the procurement process.

Directors supported further monetary policy tightening, given continuing inflation pressures.

They encouraged further action beyond tight liquidity management to rein in inflation, which would support the credibility and independence of the central bank.

While welcoming the strong banking sector performance, Directors noted that efforts to strengthen financial stability should continue, including sustaining the good progress on

implementing the 2018 FSAP recommendations.

They called for measures to increase resilience to risks stemming from high bank exposure to the Romanian state and encouraged close monitoring of the new tax on bank assets due to its potential impact on monetary policy transmission and credit allocation.

Directors also noted that the new AML/CFT legislation should be followed by a robust implementation.

Directors emphasized the need to re-energize the structural reform agenda to improve Romania’s medium-term growth prospects.

They noted that public investment should be increased by focusing on public infrastructure and achieving a more efficient absorption of EU funds.

Directors called for moving ahead with the state-owned enterprise reform agenda to improve the quality of public goods and services. They recommended moderating minimum wage hikes and linking changes to a set of objective criteria that reflect productivity.

Directors further highlighted that Romania’s fight against corruption should be renewed, noting that these reforms could alleviate constraints on growth, enhance competitiveness and facilitate investment.

(1) Under Article IV of the IMF’s Articles of Agreement, the IMF holds bilateral discussions with members, usually every year. A staff team visits the country, collects economic and financial information, and discusses with officials the country’s economic developments and policies. On return to headquarters, the staff prepares a report, which forms the basis for discussion by the Executive Board.

(2) At the conclusion of the discussion, the Managing Director, as Chairman of the Board, summarizes the views of Executive Directors, and this summary is transmitted to the country´s authorities. An explanation of any qualifiers used in summings up can be found here.