Cresterea ratei de utilizare a serviciilor bancare digitale si noua legislatie europeana privind platile (PSD2) determina bancile sa construiasca platforme tip open banking, care sa integreze serviciile bancare cu cele ale furnizorilor externi, iar Fintech-urile specializate in softurile bancare, precum Temenos, concureaza pentru a obtine noi parteneriate cu bancile.

How Temenos enables Open Banking and the Revised PSD2

Executive Summary

Open banking is the adoption of common standards for collaboration between banks and other players within the banking eco-system. This paper argues that the widespread uptake of open banking globally, accelerated by the Revised Payments Services Directive (PSD2) in Europe, will lead to new opportunities and challenges for banks. Expected to come into force by late 2018, PSD2 is intended to increase competition and innovation within the European banking industry in order to improve the banking experience for the end-customer. For this reason, it has implications well beyond Europe. Accenture has described PSD2 as an “open banking laboratory” that will be closely watched by the rest of the banking world.

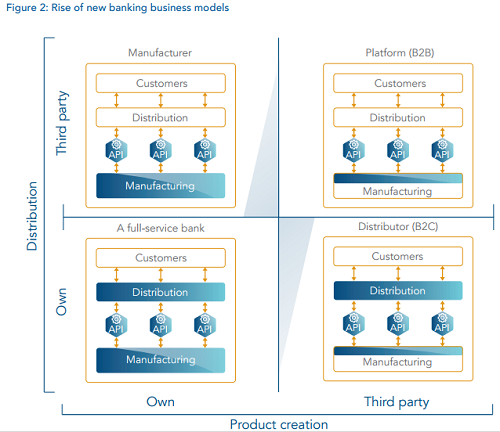

PSD2 prescribes the opening of account information to third parties, such as aggregators of customer financial information across multiple institutions, or payment providers. In order to protect themselves from the consequent risk of losing their direct relationship with customers (disintermediation), banks are likely to respond to the directive by not merely complying, but by exploiting the directive to create new business models aimed at creating new and deeper relationships with customers and at generating new revenue streams. Some banks may become account aggregators and/or crossinstitutional payment providers themselves. Others may choose to become back-office manufacturers of banking products leaving the customer relationship to others.

Beyond PSD2, open banking could lead to the rise of platform models for banking services where banks act as market intermediaries connecting customers, manufacturers and distributors. In all cases, open banking and PSD2 will place new demands on the underlying technology architectures of incumbent banks such as the need for real-time 24x7 support for open Application Programming Interfaces (APIs) and messages, performance and scalability to deal with the higher and less predictable query and transaction volumes expected, and enhanced security and authentication. Many European banks are not equipped for this change because of the limitations of their aging legacy systems. Interestingly, modern API-based architectures are beginning to appear in the industry to address these challenges, brought to market by both, agile new entrants and banks that have recently overhauled their IT landscapes.

The Temenos solution architecture enables our clients to not only be easily compliant with the directive but also to provide the necessary support for any of the new business models that our clients might choose to embrace.

Where Europe and PSD2 lead, we expect much of the rest of the world to follow, and have therefore designed our solution from a global perspective.

DOWNLOAD THE FULL WHITEPAPER

Source: Temenos website