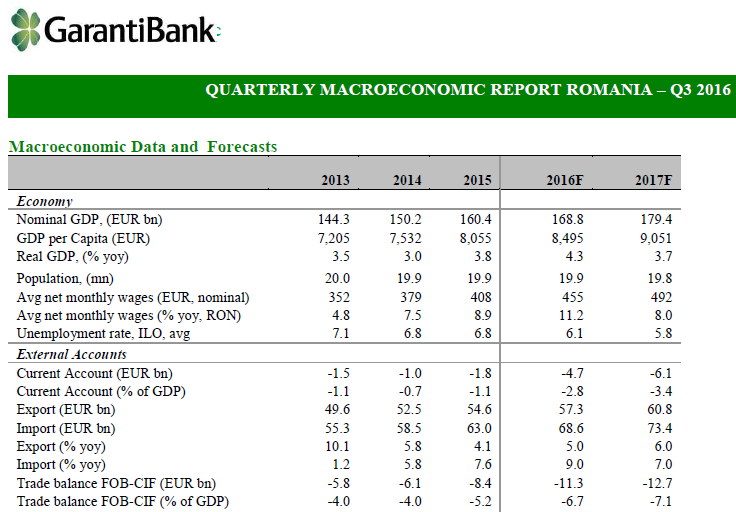

Outlook – The Romanian GDP expanded by 4.9% in the first nine months of 2016, strongly driven by private consumption amid fiscal stimulus.

Nevertheless, trade started already to decelerate in Q3 and this trend will continue for the last quarter of the year. Service sector remains the engine of the growth while the machinery and car industry just received a positive boost from external demand and a recovery is expected for the Q4.

Annual inflation in Romania is expected to end this year at zero but to enter the target band during next year. Given also the very low interest rate environment on the European level, NBR will probably keep its interest rate through the whole next year, with the first rate hike only in 2018.

At the parliamentary elections in December none of the political parties have the majority, so a coalition government will be needed. The race is quite tight and the new and smaller parties will play an important role in the negotiations for the power.

Despite some worsening of budget and external balance, macro fundamentals of Romania remain still strong. The main risk area is related to next year’s budget deficit and domestic legislative changes impacting the financial system.

Still, Romania is viewed as being stable by the rating agencies, reflected also by the relatively stable RON and CDS evolution.

The pace of lending stagnated so far. Prospects for 2017 retail lending are good, especially given the proposal to extend the First Home program by 5 years.

Company lending is still stiff, but the investment component is revived.

Main Topics:

· Politics – Parliamentary election fixed on the 11th of December

· Economic Growth – Consumption to decelerate in Q3

· Country risk profile – Stable country risk amid still good fundamentals

· Monetary stance – Low interest rate environment to persist amid historically low inflation

· Fiscal Policy and Public Finance – The budget deficit could finish the year below target

· External Accounts and Financing – The current account deficit is deepening

· Bank flows – The pace of lending stagnates, but demand for investment loans increases

See the report in Fisiere