The EU banking sector continues to struggle with high levels of non-performing loans (NPLs), low profitability and efforts to restore confidence, notwithstanding the steady strengthening of the capital base.

Nonetheless, modest asset growth continues, also supported by lower-risk traditional lending.

External events saw heightened volatility in market sentiment towards banks’ funding in the first three quarters of 2016.

Whilst funding costs have been kept low by accommodative monetary policy stances, including central banks’ asset purchase programmes, overall issuance volumes of unsecured debt were reduced in the first three quarters of 2016 compared to 2015.

Issuance concentrated on banks with a strong market perception.

Volume reductions of subordinated debt issued were particularly pronounced.

Volatility has also seen increased fluctuations in spreads for unsecured debt in 2016.

Going forward, banks will also have to take into account in their funding plans the need to meet the requirements of the global standard on total loss absorbing capacity (TLAC) and the bank recovery and resolution Directive (BRRD).

Deposit volumes have been flat in 2016. Low and partially negative interest rates have not, yet, had a negative impact on deposit volumes, but previous years’ growth has stalled.

Funding plans indicate banks’ optimism in respect of asset and liability growth. On an aggregated basis, funding plans from banks indicate they plan to increase lending to households and non-financial corporates (NFCs) by about 1 % to up to 5 % p.a. in 2016 and the two following years.

On the liability side, deposits from households and NFCs,

as well as market funding, are expected to increase for both long-term secured and unsecured funding. Expected increases are in a range between 1 % and 5 % p.a. in the years 2016, 2017 and 2018.

Seen in aggregate, it seems difficult for all banks to increase these sources of funding, especially in light of this year’s static deposit growth and volatile funding markets with several set-backs of issuance volumes.

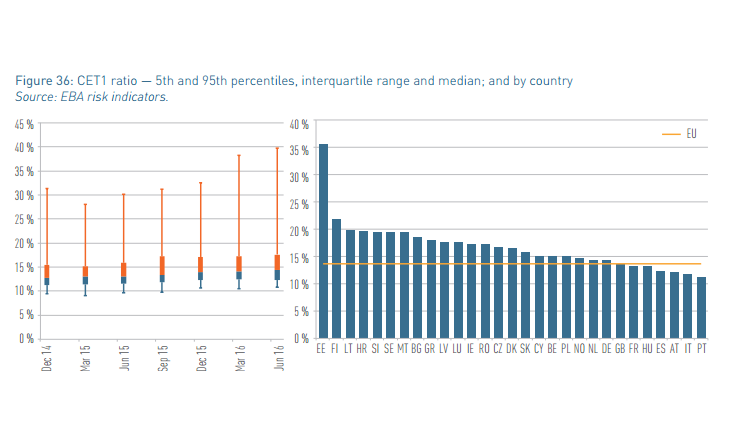

The strengthening of European banks solvency, initiated in 2011, has continued. The common equity tier 1 (CET1) ratio, computed on a transitional basis, increased by 80 basis points (bp) between June 2015 and June 2016, to 13.6 %. The fully loaded CET1 ratio was 12.1 % in June 2015 and 13.2 % in June this year.

The continuous increase in common equity is the main driver for the improvement in banks’ capital position.

Supervisory restrictions on dividends have also boosted retained earnings, despite the low profitability environment.

A downward trend in risk exposure amounts (REA) was led by a fall in credit risk as banks shifted towards lower risk weights, despite a slight increase in total assets in the same period. A fall in market risk also contributed to the decline.

Additional tier 1 (AT1) capital reached 1.2 % of REA in aggregate as of June 2016, which shows that banks still have room to further adjust their capital structure.

Only 18 % of the banks in the EBA’s sample have AT1 equal to or above the maximum amount eligible of 1.5 % for the computation of the minimum tier 1 capital ratio, whilst 75 % hold AT1 below 1 %.

Conversely, 48 % hold tier 2 (T2) capital already above 2 %, which is the maximum amount eligible for the computation of the minimum total capital ratio, while only 17 % report a share of zero. Investor demand is somewhat subdued, despite the attractiveness of higher yields, as challenging market conditions and some initial concerns about the regulatory treatment and trigger for AT1 instruments weighed on the sentiment.

Average yields for AT1 instruments were substantially

higher in 2016 compared to 2015.

A range of different terms and features observed in AT1 instruments issued in Europe and a lack of comparability may additionally have negatively affected investor interest in

these instruments.

More than one third of EU jurisdictions have NPL ratios above 10%. While there are signs of potential improvements, asset quality is still subdued compared to historical figures

and other regions.

The NPL ratio improved to 5.4 % in the second half of 2016 from 6.5 % at the end of 2014. There are still material differences in asset quality across countries.

Further gradual improvements in asset quality are expected by banks and market analysts, but they will strongly depend on successfully tackling the impediments of NPL resolution.

Profitability remains a major challenge as EU banks reported an aggregate weighted average return on equity (RoE) of 5.7 % as of June 2016, down by more than 100 bp compared to June 2015, albeit an improvement compared to 2015 and 2014 end-of-year data.

The decline in profitability was driven by a drop of total operating income by 8.8 %.

In the same period, operating expenses decreased by 3.6 %. The level of returns and efficiency as of June 2016 suggests that EU banks are not yet on a path of full recovery towards a sustainable level of profits.

It remains a source of concern in the EU banking system. This is confirmed by the fact that RoE remain below banks’ cost of equity (CoE).

Operational risks appear to be on the rise.

Information and communication technology (ICT) risk is increasing whilst litigation and conduct risk-related concerns remain. As banking operations increase their dependence

on IT platforms and telecommunication networks, concerns about connectivity and outsourcing to third party providers have

increased in prominence.

In particular, the rising digitalisation of distribution channels

and ‘always-on’ expectations of customers is putting pressure on systems to adapt.

Cyberattacks are on the rise and banks are struggling

to demonstrate their ability to cope. In this context, supervisors are focusing on ICT related risks including measures to fix rigid

and outdated legacy IT systems, IT resilience

and governance and outsourcing.

The entry of financial technology (FinTech) competitors

is also seen as a challenge and opportunity.

Banks expect compensation and redress payments to remain high. According to the Risk Assessment Questionnaire (RAQ) for

banks, over 44 % of the respondents have made compensation, litigation and similar payments of more than EUR 500 million

since the financial year 2007/08.

Banks themselves do not expect a decline in compensation

and redress payments in the near term future. Next to these potentially substantial litigation-related costs, lengthy

processes until cases of detrimental practices are settled add to uncertainties among consumers and banks.

Litigation risk is considered as one of the most important factors

negatively affecting current market sentiment for EU banks, together with regulatory uncertainty about risk weights, according to market analysts.

Challenges of NPLs, operational risks and low profitability continue to impact investor confidence in banks and impede the banking sector’s ability to contribute to economic recovery.

Action on NPLs is needed, including supervisory actions, structural reforms and development of secondary markets, along

with ongoing supervisory assessment of banks’ business model sustainability.