Standard&Poors Global Ratings affirmed its 'BBB-/A-3' long- and short-term foreign and local currency sovereign credit ratings on Romania, On Oct. 7, 2016.

The outlook is stable, said S&P in a statement.

Policy uncertainty in Romania is likely to remain elevated in the run-up to the December general elections, with possible further deterioration in public finances.

Despite the likely widening of Romania's budget and external deficits, we don't expect that government and external debt will rise significantly and think that unpredictability will subside after the elections.

We are therefore affirming our 'BBB-/A-3' ratings on Romania.

The stable outlook reflects the balance between the likelihood of Romania's twin deficits widening on the one hand, and Romania's modest government and external debt on the other.

RATING ACTION

On Oct. 7, 2016, S&P Global Ratings affirmed its 'BBB-/A-3' long- and short-term foreign and local currency sovereign credit ratings on Romania. The outlook is stable.

RATIONALE

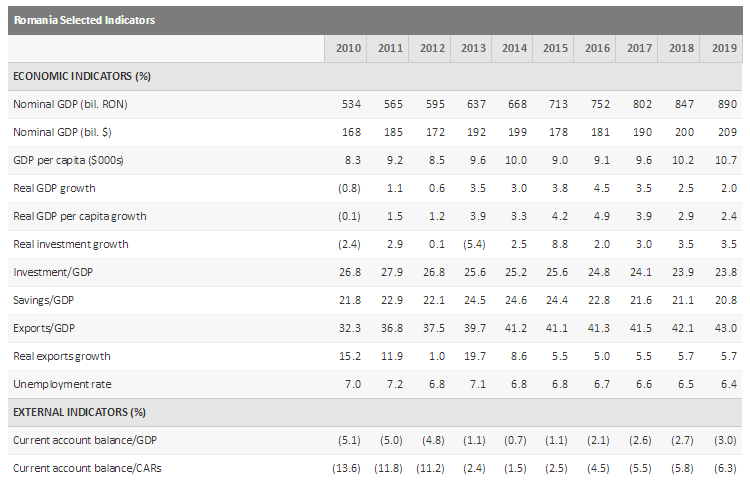

The ratings are supported by Romania's moderate external and government debt, amid reasonably firm growth prospects. The ratings are constrained by low income and wealth levels (we estimate Romania's GDP per capita at $9,100 in 2016, the second lowest in the EU), alongside a widening budget deficit and Romania's weak institutional and governance effectiveness, although we note important efforts to reduce corruption in recent years.

Romania's economic recovery--and particularly private consumption--has benefited from deep indirect tax cuts and multiple public-sector wage hikes in place since last year, alongside benign external conditions like low interest rates and oil prices.

These stimulants enabled the economy to grow in real terms by 3.8% in 2015 and 5.2% in the first half of 2016, one of the fastest rates in the EU.

We anticipate that consumption growth will remain robust until 2017 and decelerate thereafter, with an expected tightening of fiscal policy.

The resumption of the EU funds cyclewill likely support investment from 2018, in tandem with increased bank lending to the nonfinancial corporate sector.

We project real GDP will grow by 3% on average over 2016-2019.

We expect that the government's looser fiscal stance will likely push up Romania's twin fiscal and external deficits. We anticipate that the general government deficit will widen to 3% of GDP in 2016 from 0.7% in 2015.

With further measures--such as another round of cuts in value-added taxes and excise duties--due to come into effect early next year, we forecast further deterioration in the deficit to 3.5% of GDP in 2017.

Moreover, ahead of the general elections in December of this year, lawmakers are considering several legislative initiatives.

These include cuts to social security contributions, fixing the pension point to 45% of the average wage from the current 35%, and further wage hikes.

If these proposals are passed in the absence of other compensatory measures, Romania's general government deficit could widen at a much faster pace than we currently forecast.

In our opinion, fiscal policy in Romania has been historically highly procyclical, leading to large swings in demand and the performance of public finances.

With party fragmentation and a likely split of the vote on both the left and right of the political spectrum, the post-election landscape is hard to predict.

Visibility on measures to narrow the fiscal deficit is therefore low.

However, we believe that the prospect of being inducted once again into the European Commission's excessive deficit procedure should motivate policymakers to again embark on fiscal consolidation, regardless of ideology.

In this context, we think that public wage increases are unlikely to be reversed; however, investment spending could suffer.

As a result of fiscal slippage, we project that Romania's government debt burden will rise.

Still, it will likely remain moderate through 2019. We project that general government debt will reach 43% of GDP in 2019, up from our estimate of about 40% in 2016.

Over 50% of gross general government debt is denominated in foreign currency, predominantly euros, indicating some vulnerability to adverse exchange-rate movements.

Moreover, the banking system's exposure to the government equals about one-fifth of its total assets, which we believe signals reduced ability to increase exposure to the sovereign in times of stress.

Nevertheless, we note improvements in Romania's debt profile. The treasury has taken steps to lengthen the duration of its bonded debt. The average time to maturity of total debt was nearly six years in June 2016, compared with 4.8 years in December 2013.

At the same time, the sovereign's cost of borrowing has reduced, with interest expenses at 4.7% of general government revenues in 2015, down from a 5.3% peak in 2013.

Romania's external finances will likely also feel the impact of the fiscal stimulus. We project that the current account deficit will widen toward 3% of GDP in 2019 from 1.1% in 2015.

The external deficit could be larger if fiscal policy is relaxed further or the country's export competitiveness suffers from rising wages.

Romania's labor cost index rose by 10% year on year in first-quarter 2016--the fastest wage growth in the EU--after rising on average by more than 8% in 2015. Even so, the country's wage levels are well below European averages.

Romania's hourly labor costs are the second lowest in Europe, lagging all its neighbors except Bulgaria. Despite the abovementioned widening of the current account deficit, we anticipate that Romania's external indebtedness will remain moderate.

The country's external debt has diminished substantially from 2009 levels, mainly because of banking sector deleveraging.

Between 2009 and 2015, Romania's net external liabilities fell by nearly 90% of current account receipts.

We think that an improvement in energy efficiency and gradually increasing value-added in some pockets of Romania's expanding export sector--especially services--will likely prevent large external imbalances from re-emerging.

The services sector's surplus exceeded 4% of GDP in 2015, versus 1% in 2010, on the back of growth in the information technology and transportation industries.

We anticipate that, from 2018, Romania's current account deficit will be fully financed by surpluses in the capital and financial accounts.

We think the financial accounts will benefit from continuing foreign direct investment, public-sector borrowing, and slowing net outflows from the financial sector, as domestic lending opportunities increase.

Deflation, prompted by cuts in indirect taxes, is likely to persist through 2016. With very strong domestic demand, we think underlying inflation will be higher than what the headline data indicates. We also note the brisk pace of bank lending to households in 2016, with the value of mortgage loans in second-quarter 2016 increasing 16% year on year.

Much of this strong growth can be attributable to the state-guaranteed "Prima Casa" program, under which borrowers can make downpayments as low as 5% of the value of the home they are buying.

The law on debt discharge (which allows borrowers the right to discharge debt by transferring the title on a mortgaged property to creditors), passed earlier this year, has seemingly not had a marked impact on lending in this segment so far.

In contrast to retail lending, the corporate loan book continues to shrink, owing mainly to the ongoing deleveraging in foreign currency-denominated loans and the cleaning up of nonperforming loans on banks' balance sheets.

Romanian leu-denominated loans to the nonfinancial corporate sector increased by 3% year on year in the second quarter of 2016.

With most new lending in local currency, outstanding loans denominated in foreign currency, particularly euros, continue to decline, currently standing at less than 50% of the total loan book.

We believe that if this trend continues, it will likely improve the transmission of monetary policy over time, while reducing the domestic economy's vulnerability to exchange rate fluctuations.

OUTLOOK

The stable outlook reflects the balance between the likelihood of Romania's twin deficits widening on the one hand, and its modest general government and external debt on the other.

We could raise the ratings if Romania's budgetary consolidation resumed and net general government debt was firmly on a downward trajectory, including by successful restructuring or privatization of public enterprises; and if Romania's governance framework improved, translating into more predictable and

stable macroeconomic growth and government finances.

We could lower the ratings on Romania if we considered that policy reversals could cause general government deficits, debt, and borrowing costs to deteriorate significantly, or if Romania's external imbalances re-emerged.

[1]

[2]