ROMANIA

Strong growth ahead amid fiscal loosening and financial risks

Driven by wage increases and fiscal relaxation, economic growth is forecast to peak in 2016 before moderating somewhat in 2017. Inflation is projected to accelerate as of mid-2016, partially driven by wage increases.

Due to tax cuts and expenditure increases the fiscal deficit is set to increase substantially. New legal initiatives in the financial sector pose risks to the macroeconomic outlook.

Robust growth in 2015

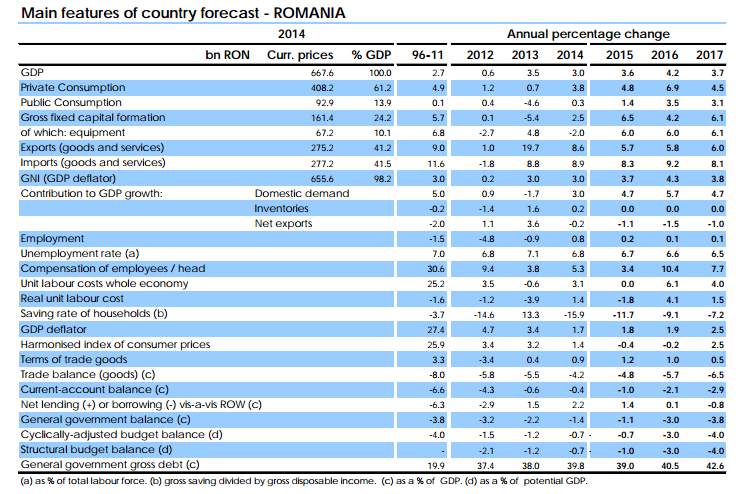

Real GDP growth in the third quarter of 2015 (3.6% y-o-y) was surprisingly strong given the significant drop in agricultural production.

The expansion was driven mainly by services, with retail trade surging after the cut in the VAT for food as of 1 June 2015, and by the ICT sector.

Private consumption is thriving, buoyed by higher disposable income and the recovery of local currency lending.

Investment has sustained its upward trend. The economic sentiment indicator reached a seven-year peak in the third quarter of 2015, pointing to continued momentum.

Real GDP growth in 2015 is thus estimated to turn out at 3.6%, its highest growth rate since 2008.

Growth to peak in 2016

Domestic demand is set to remain the driver of growth in 2016 and 2017.

The 4 pps. reduction of the standard VAT rate in January 2016 along with

negative inflation and a 19% increase in the minimum wage from May 2016 are projected to boost consumption and push growth up to 4.2% in

2016.

As inflation picks up and the fiscal stimulus fades in 2017, consumption growth is likely to slow down.

GDP growth, however, is expected to remain above potential at 3.7% in 2017.

[1]

Stable investor confidence and continued growth in local currency lending as well as the abolition of the construction tax from 2017 should help to sustain private investment growth over the forecast horizon.

Public investment growth is projected to slow down in 2016 as the absorption rate of EU structural funds dips before picking up in 2017.

Net exports' contribution to growth is projected to remain negative over the forecast horizon, as imports growth in line with surging domestic

demand outpaces exports growth.

The current-account deficit is set to widen from 1.0% of GDP in 2015 to 2.1% of GDP in 2016 and 2.9% of GDP in 2017.

Inflation to turn positive in 2016

After it dropped to a record low in August 2015, annual inflation in 2015 turned out at -0.4%, mainly reflecting the June VAT cut for food and

low global energy prices.

Brisk domestic demand growth and the May 2016 minimum wage hike are likely to exert upward pressure on prices.

This is expected to be partially offset by the 4 pps. across-the-board VAT cut at the start of 2016 and subdued oil prices.

Annual average inflation is forecast to reach -0.2% in 2016. As the impact of the VAT cuts fades out and the output gap closes,

inflation is set to return to positive territory in the second half of 2016.

It is forecast to re-enter the central bank's target band (2.5% ± 1 pp.) in 2016 and to reach an annual average of 2.5% in 2017.

Tighter labour market The downward trend in unemployment is likely to

continue, supported by strong economic growth.

The unemployment rate is projected to fall from 6.7% in 2015 to 6.5% in 2017. Conversely, employment is projected to grow over the forecast

horizon.

The 19% increase in the minimum wage in 2016 is expected to lead to higher unit labour costs overall.

The wage hike will partially offset recent gains in productivity, thereby weighing on competitiveness.

Risks tilted mainly to the downside

A major downward risk to the macroeconomic outlook is the potential implementation of the law on debt discharge as initially approved by

parliament.

The retroactive application of the law on the current stock of loans could have a negative impact on credit growth, consumer and investor confidence, and domestic demand.

Upward risks could come from a better-than-expected absorption

of EU funds and a higher multiplier effect from the fiscal stimulus in 2016 and 2017.

General government deficit set to increase

Despite robust economic growth, the headline deficit is set to rise significantly within the forecast horizon on the back of enacted tax cuts and expenditure increases.

In 2015, the general government deficit in ESA terms is expected to have declined to 1.1% of GDP from 1.4% in 2014, thanks to a robust growth of tax revenue.

Strong economic growth and enhanced tax compliance more than offset tax cuts, such as the decrease in the VAT rate for food products and in the special constructions tax.

In 2016, the headline deficit is expected to increase to 3.0% of GDP.

The standard VAT rate has been decreased from 24% to 20%, the tax on dividends has been cut, and new exemptions in Personal Income Tax (PIT) have been introduced.

On the expenditure side, public wages are set to increase considerably.

In contrast, public investment is projected to drop in 2016 and 2017 due to a slower take-up of big projects in the 2014-20 programming period of EU funding.

The headline deficit is projected to deteriorate to 3.8% of GDP in 2017 on a no-policy-change assumption.

An additional cut in the standard VAT rate from 20% to 19%, the abolition of the extra excise duty on fuel and of the special construction

tax, and further new PIT exemptions are expected to have a negative impact on revenue.

The structural deficit is forecast to increase from 1% of GDP in 2015 to 4% in 2017 as a consequence of the fiscal easing and the closing of

the output gap in 2016-2017.

Romania’s debt-to-GDP ratio is projected to rise from 39.0% in 2015 to 42.6% in 2017.

The main downward risk to the fiscal outlook in 2017 and beyond stems from an envisaged new public wage grid.